BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning

BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist

Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist  Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges

Bearish EURGBP Scenarios:

1) European growth fails to lift above 1%.

2) Stalemate in the UK-EU Brexit trade talks, which increases the risk of a no-deal exit at the end of 2020.

3) The UK government announces a much more stimulatory budget in March (the manifesto envisaged fiscal thrust of 0.4-ppt for 2020 and nothing thereafter).

4) Johnson eventually acknowledges the need for a lengthier transition period.

5) The UK government softens its stance and agrees to closer regulatory alignment to maintain frictionless trade.

Bullish EURGBP Scenarios:

1) A more substantive loosening in German fiscal policy.

2) The BoE cuts rates in January or March

3) The UK economy fails to rebound after the election.

4) A lengthy extension to the Brexit transition period beyond end-2020.

5) A re-acceleration of CB demand for EUR, potentially linked to #2 and #3.

6) Johnson refuses to soften his trade stance, leading to an even greater risk of a no deal exit at the end of 2020.

Along with the easing in global trade tensions provides strong justification for the BoE keeping interest rates unchanged at 0.75% at this juncture. However, following dovish comments from a number of MPC members recently, today’s outcome is viewed by the market as 50/50, while a full 25bp cut is priced by May. While we believe it more likely than not that the MPC keep rates unchanged, we also doubt that the message from the Committee will be sufficiently strong to alter meaningfully the market’s belief that a rate cut may be forthcoming in the near term.

Hence, our defensive stance in EURGBP has been dictated by the receding global economic tide, but we cannot ignore that political risk has been an instrumental factor in these worse macro outturns. This warrants a tactical reduction in our defensive exposure but we uphold our hedging portfolios via 3-way straddles.

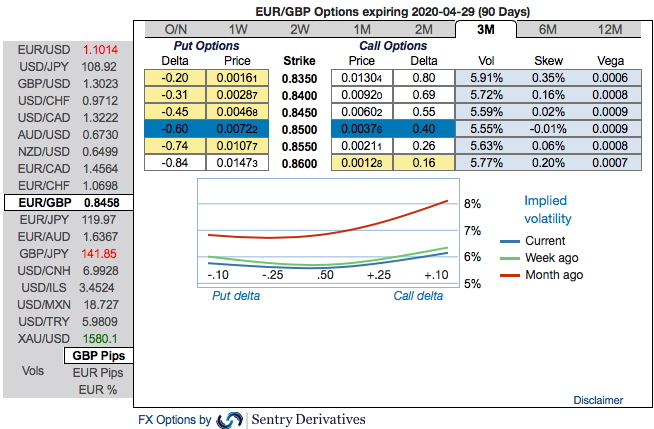

The passively skewed IVs of 3m tenors are well-balanced, indicating both upside and downside risks, more bids are observed for OTM call strikes up to 0.8350 level.

While EURGBP risk reversals of the existing bullish setup remain intact despite fresh bids for bearish risks in the short-term tenors. Below options strategy could be deployed amid the expected turbulent conditions. According to the OTC FX surface, 3-way options straddle versus ITM calls seem to be the most suitable strategy for EURGBP contemplating some OTC sentiments and geopolitical aspects.

Options Strategy: The strategy comprises of at the money +0.51 delta call and at the money -0.49 delta put options of 3m tenors, simultaneously, short (1%) ITM put option of 1m tenors. The strategy could be executed at net debit but with a reduced trading cost.

Hence, on hedging as well as trading grounds, initiate above positions with a view of arresting potential FX risks on either side but slightly favoring short-term bearish risks. Courtesy: Sentry, Saxo & JPM