UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate

Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data

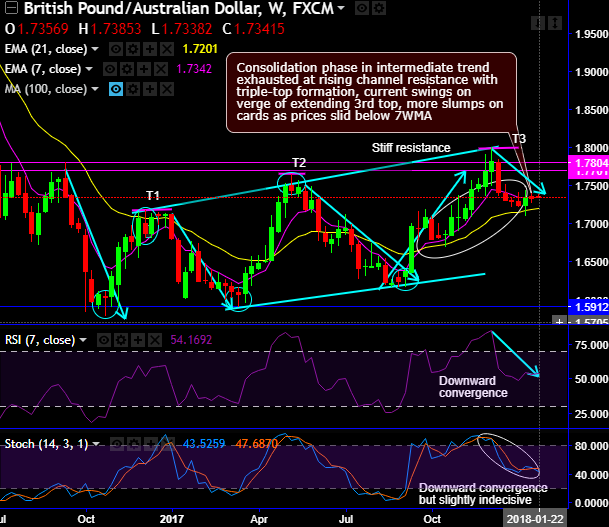

Bearish sterling scenarios:

1) UK growth stay nears 1.5%.

2) CPI peaks and wage growth fails to accelerate to 3%;

3) The balance of payments pressure (capital repatriation from LT investors; current a/c stuck at 4-5%). 4) PM May faces a Conservative leadership challenge.

Bullish sterling scenarios:

1) The economy rebounds to 2% on stronger export demand and the curve prices 2 hikes by end-18. 2) The EU softens its stance towards a FTA that incorporates services.

Bullish AUD scenarios:

1) The unemployment rate moves back towards 5.75%, raising risks that the RBA responds to a weakening labour market;

2) China data weaken materially; or

4) The risk markets retrace and vol rises as financial conditions tighten.

Bearish AUD scenarios:

1) China eases policy and commodities rebound;

2) The Fed’s tightening timeline is severely disrupted by further downside surprises on inflation; or

3) The RBA adopts a more hawkish tone to its communications.

Hedging strategy:

3-Way Options straddle versus Call

Spread ratio: (Long 1: Long 1: Short 1)

The execution: Initiate long in GBPAUD 3M at the money -0.49 delta put, long 2M at the money +0.51 delta call and simultaneously, short theta in 1m (1%) out of the money call with positive theta or closer to zero.Theta is positive; time decay is bad for a buyer, but good for an option writer.

Rationale: Please be noted that 3m skews are stretched on either side, ATM options have more likelihood to expire in the money and the 1m IVs are just shy above 8.12%, whereas 1% OTM calls of this tenor seem to have been overpriced at 18.75% more than NPV, hence, we foresee writing such exorbitant calls amid bearish pressures are beneficial as there exists the disparity between IVs and option pricing.

Hence, we encourage vega longs and short thetas in the non-directional trending pair but slightly favors bearish strategy as the vega signifies the sensitivity of an option’s value owing to a shift in volatility. It is usually expressed as the change in premium value per 1% change in implied volatility.

FxWirePro launches Absolute Return Managed Program. For more details, visit: