Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning

Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning  Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure  BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow

BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow

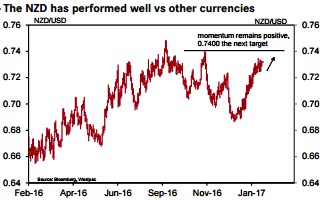

The sharp rise in NZDUSD during the past month continues to reflect the pullback in the US dollar as well as continuing strength in the NZ economy. The November high at 0.7400 is now vulnerable, and should that break then 0.7485 will be in sight (refer above chart).

This Thursday we have the RBNZ’s MPS. It should cause few ruffles in the market, with the policy stance (on-hold with a neutral bias) likely to be retained. That is because the positive impulse from dairy prices is roughly offset by the higher NZD TWI and higher funding costs. The RBNZ’s OCR projection should remain unchanged at 1.7%.

However if there is a risk of it shifting it would be in an upward direction. Should that occur, markets will feel emboldened to price in rate hikes even more aggressively than the 100% chance of one in November.

The RBNZ inflation expectations survey, just released, surprised markets with a healthy jump from 1.68% to 1.92%. At the margin, this could impart a slightly hawkish tone to Thursday’s press release.

The GDT dairy auction (Tonight) is predicted by futures to result in a 1.5% fall in WMP prices, which should be trivial if proven true (refer above chart).

Speculative positioning in NZDUSD, proxied by CFTC futures positions of leveraged and non-commercial trader types, indicates longs are starting to be rebuilt and are at the highest level since November (refer above chart).