BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning

BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning  How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform

How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform  China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven  Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings

Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings  BOJ Expected to Hold Rates Steady While Signaling More Hikes Ahead

BOJ Expected to Hold Rates Steady While Signaling More Hikes Ahead  Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates  Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

Long EURJPY is a strategic view on the sequencing of central bank policy. The ECB remains on the cusp of tapering, even if Draghi would not commit this week to a particular meeting for that decision to be taken, over and beyond flagging the autumn.

Meanwhile, the BoJ is resigned to waiting yet another year before it expects to achieve its 2% inflation objective, with its best guess now being that mission will not be accomplished until FY19. In recent weeks, the G10 (ex. Japan) long-end yields have risen sharply due to heightened speculation on policy normalization spurred by a series of hawkish commentaries from central bank officials.

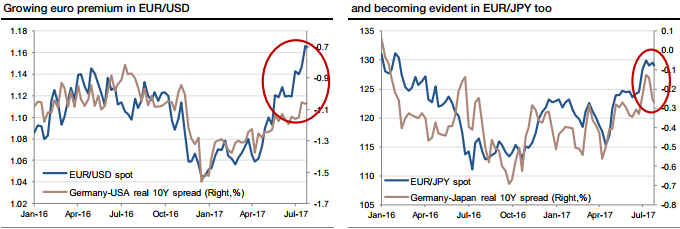

Real yield spreads in both EURUSD and USDJPY have supported a weaker dollar. That being said, it is becoming apparent that there is a growing euro premium, which can be seen even in the EURJPY cross in recent weeks (refer above charts). While the divergence in the thrust of policy seems clear enough and also relatively persistent, we'd acknowledge that EURJPY bulls are now in the majority and that crowded spec positions could slow the extension in the spot in the low 130s.

This set-up favors holding short gamma overlays to core long positions, for instance through ratio call spreads or, in our case, a call RKO.

Bought EURJPY at 128.50 on July 4th. Marked at 0.84%.

Bought a 2m EUR call/JPY put, strike of 133 RKO 137 for 21bps on July 7. Worth 12.5bp.