Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be

Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

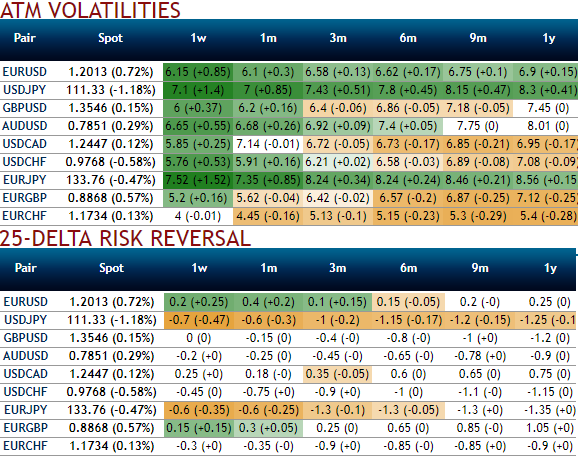

The global picture on the volatility front hasn’t really changed in recent months. Implied and realized volatility is still hovering in their low or very low percentiles.

The currency market has been acting as the adjustment factor between countries positioned at different parts of the economic cycle clock. Please refer above nutshell that evidences depressed volatility keeping entry costs low while uncertainty is still lingering the probability of a positive return. Japan and core euro zone are our preferred markets.

It has been one of the few assets on which carrying long volatility positions has not been a constant pain. It has also led to a dramatic reversal in the correlation regime, leading to some significant discounts on equity options contingent to currency levels.

The fundamental motivation for owning GBP volatility was straightforward and colored by uncertainty on multiple fronts – around the Brexit process, increasingly dysfunctional domestic politics, continued debate around the abrupt change in the BoE’s reaction function and the risk of an unwind of rate hikes priced along the yield curve should growth and/or politics intercede.

With current levels of implied vols still low, we continue to find value in holding this trade.

Long a 1Y vol swap in EURGBP. Opened at 8.85%November 21. Marked at 8.15%.

Elsewhere, even though not explicitly an Outlook 2018 theme, we had spotted out and highlighted the luring factor of owning CAD-denominated correlations, specifically CADUSD vs CADJPY as a positive carry NAFTA hedge in December. CAD and MXN have already proven relative outperformers since then amid the broad-based softness in vols elsewhere (refer above chart), which allied with the collapse in USDJPY vol has helped this trade: realized CADUSD – CADJPY corrs have clocked almost 20 points over implieds since publication, and there is value still to be extracted from CADJPY vs USDJPY vol spread.