Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  3 clinical-grade skincare creams you really shouldn’t buy online

3 clinical-grade skincare creams you really shouldn’t buy online  BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow

BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

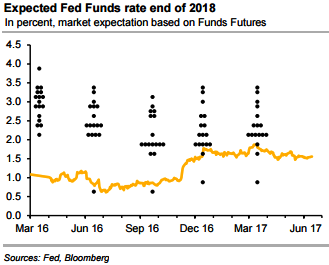

The old conflict between what the market expects and what the Fed suggests has been re-ignited. This does not involve a rate hike expected for today which is completely priced in on the market and which therefore constitutes a non-event.

So, what is decisive for USD is the monetary policy outlook beyond today. And that is what Fed and market do not agree on, as the rate expectations until late 2018 illustrate (refer above chart).

Over and beyond today’s 25bp rate hike the Fed expects four further rate steps until the end of next year, the market only one or two.

DXY (US dollar index) which measures the greenback’s strength against a trade-weighted basket of six major currencies, was steady at 96.99. It has been trading in the choppy range from the last couple of days, having no proper direction of the trend with slightly bearish bias.

Ahead of today’s FOMC’s decision on funds rates, although we could see some sort of bearish sensation but the swings could go in either direction with the major trend goes in consolidation phase. Hence, the recommendation goes this way:

Initiate long in 2w ATM +0.51 delta call, and simultaneously buy ATM -0.49 delta put of the same tenor for net debit.

Well, this option trading strategy that is used when the options trader ponders that the underlying gold prices would experience significant volatility but not sure of the direction of the swings.

The overnight volatility has two readings, which are necessary and complementary to read risk event premiums. The directional purpose is related to the straddle breakeven, while the volatility purpose is linked to the realised intraday volatility.

Directional o/n vol: minimal spot return at the end of the day. Volatility is a concept that does not assume a rise or fall in spot, but only the size of the moves. This is why it is relevant to consider potential spot moves either way, which correspond to the breakevens of a straddle (refer above graph). When investors buy an o/n straddle with a directional purpose, they are ready to pay its implied volatility only if they expect the spot to move beyond one of the breakevens. So the implied o/n volatility embeds the minimal spot move that directional investors expect on that day.