S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  ‘Vibe coding’ is fun and easy, but there’s a major catch

‘Vibe coding’ is fun and easy, but there’s a major catch  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

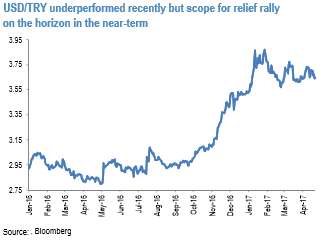

Among EMFX we stay MW TRY in the GBI-EM Model Portfolio, the resolution of uncertainty after last week's referendum opens the door for a relief rally in the short-term, but medium term concerns remain; stay MW TRY in the GBI-EM Model Portfolio. The Turkish referendum last weekend was in line with our expectations.

The package of constitutional amendments was approved by a weak “yes” (51.4% approval vs 48.6% reject, according to the latest available data from unofficial results). The opposition party CHP’s appeal on the referendum result has also been rejected by the Turkey election board. This result is the most market-friendly outcome by tapering the political noise for the time being.

Judging from recent comments by the Turkish officials, early elections this year are very unlikely and therefore the political risk calendar for the remainder of the year is light. With the weight of political uncertainty no longer bearing down on Turkish lira assets, we think there is scope for a relief rally in the currency over the short run given its significant underperformance in recent months (refer above figure).

Medium term, however, we remain MW TRY in the GBI-EM Model Portfolio as the lira is likely to resume a depreciation trend later in the year when the central bank unwinds its tight liquidity policy.

Outright trades:

On hedging grounds we advocate following FX derivatives trades:

Short EURILS via mid-month forwards.

Long 26-Apr-17 EURPLN call (4.25), spot ref: 4.200.

Short 27-Nov-17 EURCZK forward.