Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning

Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  3 clinical-grade skincare creams you really shouldn’t buy online

3 clinical-grade skincare creams you really shouldn’t buy online

In today's NBP meeting, just like the NBR, has been a status quo event. There had been some likelihood earlier that the Polish central bank might change its rhetoric or assessment because inflation was beginning to accelerate and rising energy prices, globally, were a risk factor.

The National Bank of Poland held its benchmark reference rate at a record low of 1.5 percent on October 3rd2018, as widely anticipated. We already observed euro zone inflation surprise to the downside for September and this week, Polish inflation did so too – the headline inflation rate dipped back from 2% to 1.8%, and calculations suggest that the core inflation rate dipped too. With underlying inflation running only at c.1.4% at the moment (CB inflation target: 2.5%), we do not see any reason why NBP would change its stance or assessment today.

We like the following expressions of short EM and/or high- beta G10 FX vol:

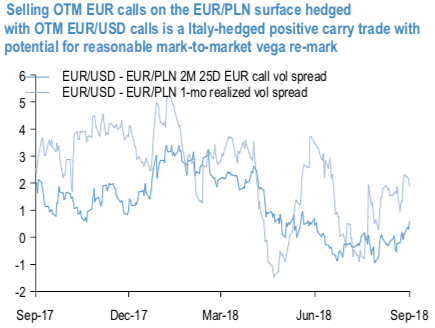

OTM EURPLN calls: Our EMEA team has a constructive take on the zloty, which is a first order source of comfort for vol sellers. Exposure to a slow burn recovery in the Euro area, strong domestic dataflow that has anchored growth forecasts at an impressive 3.8% pace for 2H’18 and revival of FDI inflows are FX positives that should promote PLN outperformance vis-à-vis regional EM peers.

On the vol side of things, EURPLN risk-reversals have been elevated for a while (SABR implied spot-vol corr for 3M riskies 42%), but it is only in the past couple of weeks that realized spot-vol corrs have plummeted (10-day spot-3M ATM vol corr. -20%) and created genuine value in shorting OTM EUR calls on the surface. This is better done in shorter rather than longer maturities given the flatness of the vol curve.

For instance, 2M 25D EUR calls at 6.3 vol are priced at a 1.5 vol premium to trailing 1m realized vol.

Taking advantage of this richness via short EURPLN – long EURUSD option spreads using OTM EUR calls. The rationale is two-fold:

a) Neutralization of Italian budget risks inherent in selling EUR-cross options; and

b) The long vol hedge is efficient on a standalone basis and does not detract from core short vol P/L: in contrast to the EURPLN surface, OTM EUR calls are priced at a discount on the EURUSD surface, and gamma is much firmer. The net result is a positive carry vol spread construct that has decent potential for mark-to-market gains from a re-pricing of implied vols (refer above chart). Courtesy: JPM

Currency Strength Index: FxWirePro's hourly EUR spot index has shown -94 (which is bearish), while hourly USD spot index has shown 97 (bullish), while articulating at 13:25 GMT.

For more details on the index, please refer below weblink: