How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum

Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

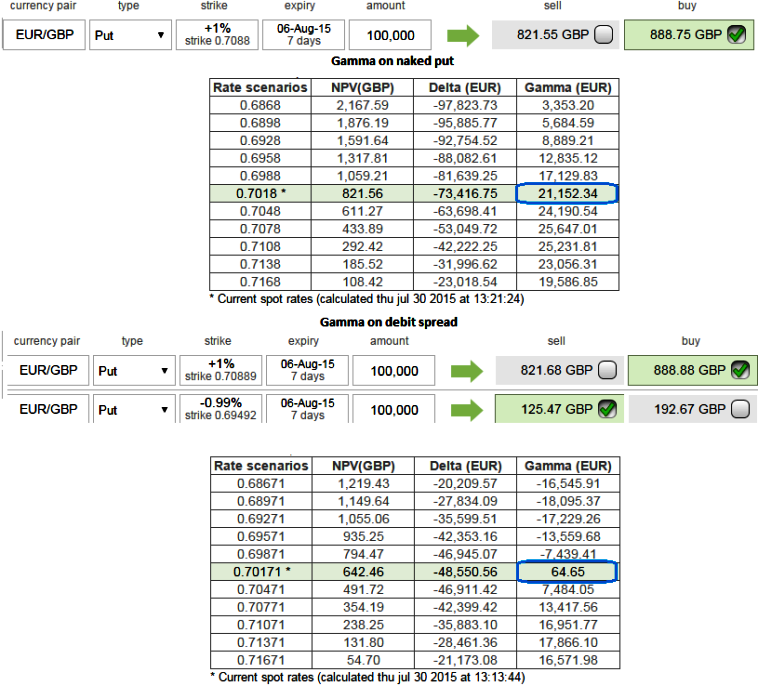

Hedging framework using naked contracts would turn out to be a gamble on highly volatile currency pairs (EURGBP and EURUSD are the ones among the pool), it may fetch desirable outcomes but at times seems unlikely irrespective of mathematical computations, hence a lot of spreads have been drawing up some customized strategies by using P&L tools and techniques while looking upon the option Greeks and technicals.

While doing so it seems like the FX options involving euro have tons of Gamma. It might be puzzling because on one hand it seems some of these options are highly volatile than any other euro currency pairs but a tiny shift in the underlying exchange rate would cause instant disaster. This can be arrested by devoting little time on ascertaining an accurate gamma.

As you can observe from the diagrammatic representation, we've constructed put spread by considering gamma closer to zero would neutralize the implied volatility impact on option price and this position remains quite firm to achieve our hedging objectives, because we know gamma represents the change in delta, we have healthier delta at 0.38.

This results in desired hedging objective irrespective of implied volatility disruptions as we've OTM shorts on side and prevailing bull run will be taken by In-The-Money calls.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: EURGBP volatility optimizer through gamma spreads

Thursday, July 30, 2015 7:59 AM UTC

Editor's Picks

- Market Data

Most Popular