FxWirePro : EUR/NZD holding below 38.2% fibo ahead of US data

FxWirePro : EUR/NZD holding below 38.2% fibo ahead of US data  FxWirePro: GBP/USD rises as weak U.S. jobs data pressures dollar

FxWirePro: GBP/USD rises as weak U.S. jobs data pressures dollar  FxWirePro : USD/CAD falls as strong Canadian jobs data lifts loonie

FxWirePro : USD/CAD falls as strong Canadian jobs data lifts loonie  FxWirePro: USD/ZAR gains some ground, but downtrend remains

FxWirePro: USD/ZAR gains some ground, but downtrend remains  FxWirePro: USD/CNY slips as strong China exports data Lift yuan

FxWirePro: USD/CNY slips as strong China exports data Lift yuan  FxWirePro: USD/JPY holds tight range ahead of key U.S. payrolls data

FxWirePro: USD/JPY holds tight range ahead of key U.S. payrolls data  Major Pair Currency Score: NZD/USD and AUD/USD Lead Forex Rally with Perfect 100 Scores

Major Pair Currency Score: NZD/USD and AUD/USD Lead Forex Rally with Perfect 100 Scores  DAX & CAC40 Score Perfect 100: Extremely Bullish With Major Levels to Watch as FTSE100 Hits 80

DAX & CAC40 Score Perfect 100: Extremely Bullish With Major Levels to Watch as FTSE100 Hits 80  FxWirePro- Major Crypto levels and bias summary

FxWirePro- Major Crypto levels and bias summary  EURGBP Bears Break Trendline: Sell Rallies at 0.8578 as Support Breach Eyes 0.8450 Slide

EURGBP Bears Break Trendline: Sell Rallies at 0.8578 as Support Breach Eyes 0.8450 Slide  FxWirePro: NZD/USD retreats as Middle East instability weighs

FxWirePro: NZD/USD retreats as Middle East instability weighs  Bitcoin Reclaims $65,000 as Easing Geopolitical Tensions Fuel Risk-On Rally

Bitcoin Reclaims $65,000 as Easing Geopolitical Tensions Fuel Risk-On Rally  NZDJPY Bears Lie in Wait: Sell Rallies at 93 for 90 Target with 94 Stop

NZDJPY Bears Lie in Wait: Sell Rallies at 93 for 90 Target with 94 Stop  FxWirePro: GBP/AUD eases slightly, focus on near-term support

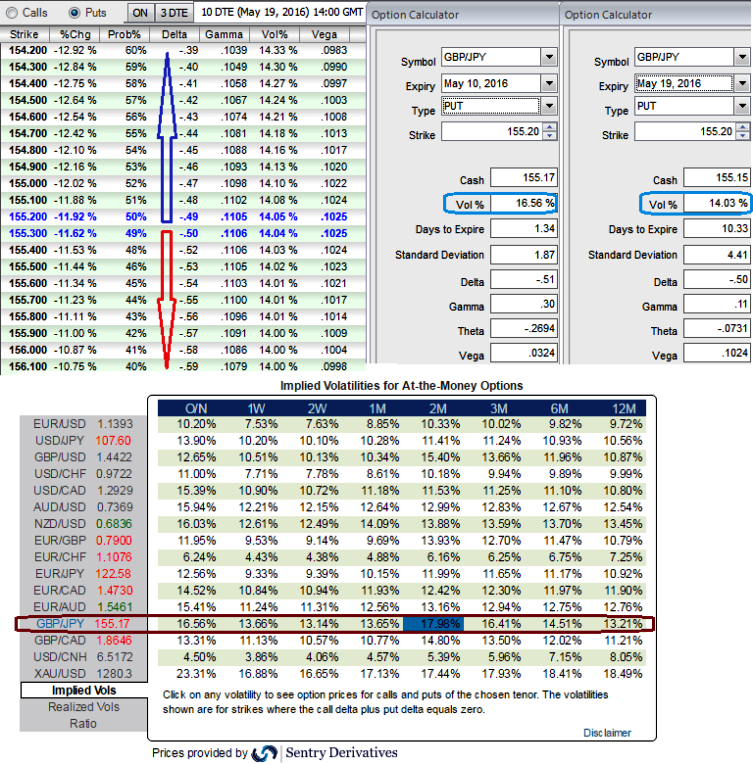

FxWirePro: GBP/AUD eases slightly, focus on near-term support

The Sterling and Yen remained in a holding pattern ahead of today’s BoE’s monetary policy, trade balance in UK and current account in Japan.

ATM IVs of 1D and 1W expiries are at 16.56% and 13.66% respectively.

IVs of 13.65% & 17.98% for 1M and 2M tenors respectively, so it has reduced a bit, however the volatilities implied in FX option market of this pair is likely to perceive lower volatility times even during UK’s monetary policy which is good news for option writers.

Vega is usually expressed as the change in premium value per 1% change in implied volatility.

Now, let’s glance on the sensitivity table for %change in every rise in GBPJPY OTM strikes, probabilities and their corresponding vega values, fluctuations on either side about 50 pips would not differ much in vega numbers despite the reducing IVs which means that higher chances of both ITM and OTM strikes of 50 pips expiring in the money are very high.

But, the volatilities would likely favour option writers as they are likely fade away.

Subsequently, have glance on sensitivity table as well for the different rate scenarios and their probabilistic outcomes. We've just referred 0.25% OTM put strikes and their vols, it still shows 0.47 as delta values for underlying outrights with 52% of probabilities, that means 52% chances of finishing in-the-money.

Usually, the options of ITM strikes are the most expensive, so buyers would pay the most and sellers would receive the most. Their premium is mostly made up of intrinsic value so they are relatively immune to Vega and Theta.

Vega is stagnant on either side, hence, trade an ITM option if you want to minimize the risk of Vega and Theta. They are an excellent tool when you have a strong view on the market because deep ITM options have the highest Delta. They will behave more like a position in the underlying.

On the flip side, OTM options are always the cheapest options hence buyers pay less and sellers receive less. They rely solely on extrinsic value and have a low Delta, Theta, and Vega. A move towards the ATM territory increases the Vega, Gamma and Delta which boosts premium.

Hence, OTM put options are the best suitable for those we seek long term hedging instruments for further downside risks and ITM options for short term.