Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data

After yesterday’s weaker than expected, UK services PMI reading, the GBP and UK yields have been observed under pressure ahead of the BoE tomorrow. We have no data today, with PM May in Northern Ireland for a second day. Yesterday, she said that while a changed ‘backstop’ was a key issue in the Brexit process, she retains an ‘unshakeable’ commitment to avoiding a hard Irish border. Moreover, while she believes that technology can play a part on the border, it must be workable.

FX market participants with GBP exposure are not very interested in statements about likelihoods. All outcomes are sufficiently likely to require participants to be prepared. The speculative market participants whose portfolios are widely diversified and who therefore can apply probability statements stand to attention ready to bet on the GBP recovery, which can be expected in case of a constructive outcome.

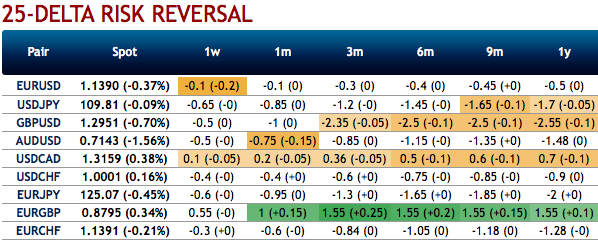

However, that should not prevent the market from reflecting the changing likelihood of “no deal” proportionately in the GBP exchange rates. That does not happen the whole time, and when it does happen it happens in bursts – as was the case yesterday when Sterling eased on the back of not-so-surprising PMI data. Does that mean that the no deal risk is reflected adequately in the GBP exchange rates this morning? Even the asymmetry of the risks is priced into the exchange rates to a very limited extent with 3M 25-delta risk reversals around 1.50 percentage points (given that 3M ATM vol trades around 10.1%) compared with the market reaction following the Brexit referendum in 2016.

The fresh negative bids in the shorter tenors have been observed to the bearish risk reversal atmosphere in the GBP OTC markets, this is interpreted as the hedgers are keen on bearish risks in the broader perspective.

You could easily make out that the positively skewed IVs of GBP have been stretched out on the downside. Mounting bidding for OTM puts is interpreted as the hedgers’ interests for the downside risks (refer above nutshells).

It is tough to believe either that the UK would be suffering any food shortages in case of “no deal” and expect that Brits will still be able to fly to Spain for their vacation trips. Anyone banking on horror scenarios is likely to fall flat on their face.

However, it is likely to be days or weeks between the news that there is going to be a no deal Brexit and the realization that even in that case Great Britain is not going to be swallowed up by the ground. Quite a few analysts consider the GBP weakness during this time frame to be sufficiently priced in. Courtesy: Sentrix, Saxo & Commerzbank

Currency Strength Index: FxWirePro's hourly GBP is at -28 (mildly bearish), hourly USD spot index is inching towards 114 levels (bullish), while articulating at 14:49 GMT.

For more details on the index, please refer below weblink: http://www.fxwirepro.com/currencyindex