Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation

SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform

How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be

Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be

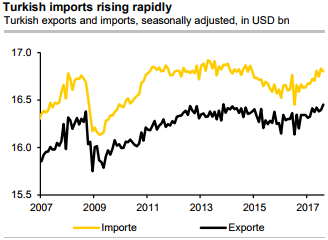

We’ve seen the trade and tourism data for August on Friday: the trade data highlight continuing widening of the trade deficit despite healthy export growth -- both exports and imports have accelerated visibly during the past couple of quarters, but imports have accelerated more (refer above chart), driven by rising demand as well as rising price of crude oil.

The deficit as a percentage of GDP has widened out quite sharply, going from c.7% of GDP just a quarter ago to 8.5% now. The data support our forecast of a wider current-account deficit this year than last year - this is the usual pattern when the Turkish economy grows faster, but usual or not, a wider deficit seems unsupportive for lira.

On the tourism side, foreign arrivals in August were closer in line with the seasonal average from past years - this picture is similar to what we saw in July; tourists from the CIS made up 34% of the total, tourists from EU made up 41%. From the lira's point of view, we interpret the trade data to be negative, the tourism data to be neutral.

On the flip side, the Turkish lira has been trading vigorously in the recent months and it has continued its robustness through August but September has been little edgy, although its performance has been far more impressive against the ultra-weak USD than against the basket (made of half USD, half EUR).

Against a favorable backdrop for continued yield-seeking behaviour, TRY looks attractive for its cheap valuations (16% under-valued versus 10-yr REER average), CBRT’s commendable shift toward tight monetary policy and prioritization of financial stability, and the country’s diminished risk of political upheaval. November 2019 general elections provide motivation for officials to bolster economic momentum while keeping the currency stable.

The driving forces: Perpetuation of suppressed reflationary risks in developed markets support TRY as a high-yielding EM currency. A clear decline in locals’ appetite for accumulating FX deposits (some timid initial signs have appeared) could spark the next leg of the TRY rally.

Hence, we advocate below options strategy on hedging grounds amid the mixed bag of fundamental drivers.

Options Strategies (USDTRY):

The conservative hedgers can prefer the below strategy:

Debit Put Spread = Go long 1M ATM -0.49 delta Put + Short (1%) OTM Put with lower Strike Price of similar tenor with net delta should be at -0.14.

For a net debit bear put spread reduces the cost of trade by the premium collected (on the shorts of OTM put) and keeps option trader to participate in downward moves and any upswings in abrupt.

Moreover, the risk is capped to the extent of initial premium paid, as opposed to unlimited risk when short selling the underlying outright.

However, put options have a limited lifespan. If the underlying FX price does not move below the strike price before the option expiration date, the put option will expire worthless.

Alternatively, aggressive bears can bid USDTRY 1% OTM strikes of naked put with mid-month tenors.