Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch

The implied volatilities of crude oil options have dropped considerably on the back of last week’s OPEC production cut pact. For an instance, the 3m at the money WTI implied volatility has dropped a massive 10 percentage points to about 33% since the OPEC announcement to cut output by 1.2 Mb/d. As we have mentioned before, we believe that the return of OPEC to active supply management is like to result in 3m implied crude vols trading below 30% to around 25% over time.

Crude stocks drew by 2.4 Mb (vs. -1.5 Mb expected), while Cushing saw a 3.8 Mb build (vs. +0.3 Mb expected). Imports jumped by 755 kb/d to 8.30 Mb/d, back from relatively low levels the preceding two weeks. Refinery runs rose by 134 kb/d to 16.42 Mb/d, while 4w av. runs declined by 172 kb/d to 16.31 Mb/d (-1.0% y-o-y). Production was flat at 8.70 Mb/d, with lower 48 output edging down by 2 kb/d. Stocks remained far above 5y highs.

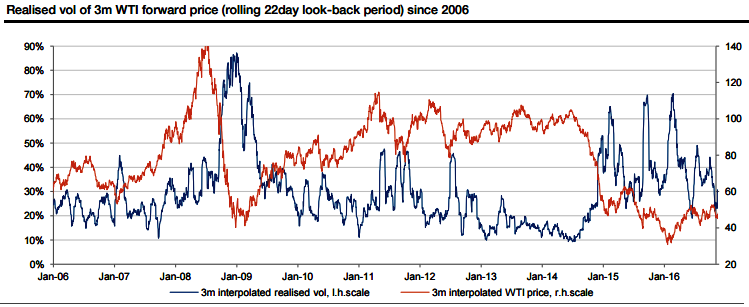

The chart above shows the daily realized vol of the 12-month WTI forward price since 2006. We believe that 2017 will share similarities with the 2010/11 period when the oil market was recovering from the 2008/9 oversupply helped by OPEC cuts.

Back then, the 3m realized vol dropped below 30% during most of 2010 and H1’2011. Please note that the realized vol in the chart is calculated using a rolling 22-day look-back period.

The short (but standard) look-back period makes the realized vol quite volatile. The 3m implied vol tends to be much less volatile than the 3m realized vol using the standard 22-day look-back period.

Despite the OPEC deal and the jump higher in oil prices, consumer hedging activity has remained muted while producer hedging, mainly by US producers, has continued. This suggests that the longer-dated risk-reversals will remain very skewed with the implied vols of out-of-the-money puts trading well above out-of-the-money calls. Indeed, the 12-month WTI and Brent 25-delta risk-reversals (put minus call) are trading at multi-year highs.