How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform

How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform  Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war  ‘Vibe coding’ is fun and easy, but there’s a major catch

‘Vibe coding’ is fun and easy, but there’s a major catch  BOJ Expected to Hold Rates Steady While Signaling More Hikes Ahead

BOJ Expected to Hold Rates Steady While Signaling More Hikes Ahead  Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields

Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields

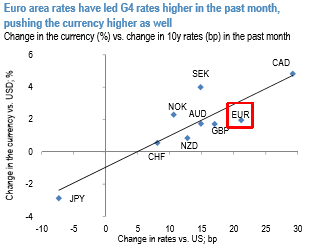

The ECB has signaled a taper announcement for September, while the Fed has been noncommittal on the timing of balance sheet normalization, prompting a Bund-led rise in DM yields which has been EUR supportive (refer above chart).

Well, it’s ECB today..! President Draghi is expected to signal a dovish tightening. Managing the communication will not be easy; at the same time seeking to maintain market expectations that policy normalization is underway, but also avoiding another bond sell-off and euro appreciation.

The base case is for the ECB to announce taper at the September meeting.

While we expect the Fed to announce balance sheet normalization in September as well, the Fed has refrained from sending a firm signal on timing thus far.

The bearish forecast reflected the view that the ECB would be quieter on the taper in the near-term.

Moreover, markets appeared better prepared for an ECB taper than for the onset of Fed balance sheet normalization, as reflected by already-long EUR positions and overshooting valuations vs rates, so any rise in yields was expected to be led by the US.

Hence, a more activist ECB warrants a modest upgrade to the EURUSD forecast, long-standing medium term forecast has been bullish (4Q at 1.15 and 2Q18 at 1.16), while our near-term forecast was bearish (3Q EURUSD target was put at 1.08).