Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940

Gold Slips Below $4050 as Bond Yields Surge to 4.7% on Fed Inflation Concerns – Sell Rallies at $4060 Targeting $3940  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate

Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate  3 clinical-grade skincare creams you really shouldn’t buy online

3 clinical-grade skincare creams you really shouldn’t buy online

No doubt from last two weeks, USDCNY has been spiking higher to the current levels of 6.5954 from the recent lows of 6.4345 levels.

However, it is foreseen that the strength of CNY can be traced to three factors:

The rebound in real GDP, higher commodity prices (which has aided the reflation theme and reduced pressure on the banking system) and higher interest rate differentials.

At the same time in recent months, our proxy of FX positioning data indicates that Chinese corporate USD selling interest has risen noticeably.

To the extent that this positioning adjustment is not yet complete suggests we could still further downside pressure in USDCNY in the near term.

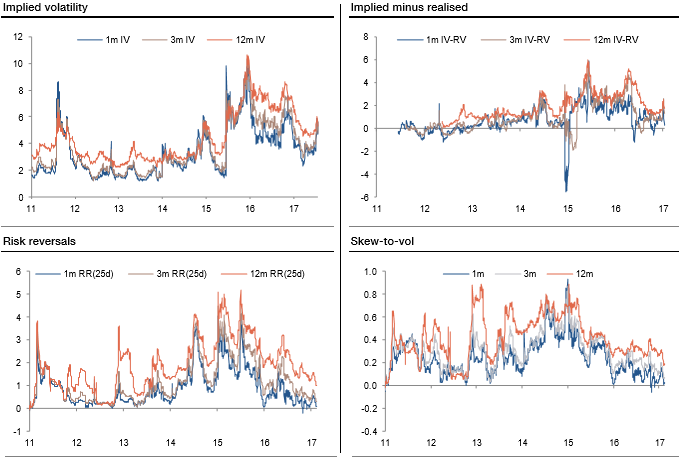

The implied volatility has bounced off the recent lows, the richness of implied versus realized vols has eroded; risk reversals and skew-to-vol are falling, term premiums have compressed while the vol smile has moved higher.

The base case scenario envisions CNH outperforming the forwards to year end.

However, a near term correction might ensue if EUR/EM FX falls or the Party Congress disappoints on the growth front. The PBoC has shown unease about USDCNH being much below 6.50. Topside exposure coupled with selling a downside strike (i.e. bullish seagulls) could be an appropriate structure.