U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations

Japan Services Producer Prices Rise 3.2% in June, Supporting BOJ Rate Hike Expectations  BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow

BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions

Fed Holds Interest Rates Steady as Kevin Warsh Says Rising Treasury Yields Tighten Financial Conditions  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  BOJ Expected to Hold Rates Steady While Signaling More Hikes Ahead

BOJ Expected to Hold Rates Steady While Signaling More Hikes Ahead  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

In this write-up, we emphasize on the disparity between the NZD IV skews and the long-term underlying projections. Well, please be noted that 1w IV skews of NZDUSD have been stretched on either side (refer above nutshell, it signifies both upside and downside risks ahead of RBNZ’s monetary policy meeting for its OCR, which is scheduled on November 7th), both OTM call and OTM put strikes have equal chances of expiring in-the-money.

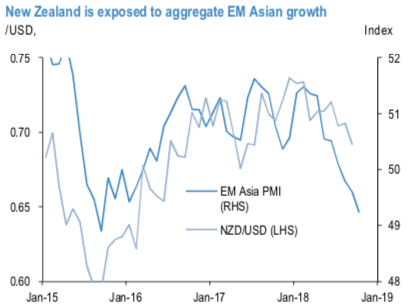

Whereas Kiwis dollar’s (NZD) weakness has been prolonged in sympathy with high-beta FX. This led us to slightly lower our NZD forecasts last month to reflect risk of ongoing negative news-flow relating to EM. In contrast to Australia, where the export-relevant commodity markets are already tight, New Zealand is unlikely to benefit from a redistribution of China’s GDP growth toward fixed asset investment. Rather, its mostly agricultural export basket is more exposed to softer EM Asian growth in aggregate (refer 1stchart).

The projections for NZD to end 3Q’19 at 0.61. There have also been important domestic drivers of NZD’s slide this year. The RBNZ has maintained dovish rhetoric, despite the fact that the 2Q GDP data came in better than expected. Looking at annual rates, GDP growth clearly has slowed, relative to the bullish rates that prevailed at the immigration peak over 2014-16. This is significant given that even over that extremely strong window for growth, the central bank struggled to lift inflation (refer 2ndchart).

RBNZ Governor Orr has highlighted that the OCR will need to be on hold until 2020, in order to push growth back above 3%. As with AUD, we expect ongoing confirmation that the central bank can credibly lag policy normalization in the G3, which should see the currency sustain recent devaluation even if EM outflows stabilize.

Currency Strength Index: FxWirePro's hourly NZD spot index is inching towards 113 levels (which is bullish), hourly USD spot index was at 10 (neutral), while articulating (at 13:22 GMT). For more details on the index, please refer below weblink: