Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be

Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation

What a difference a month has made to GBP in terms of immediate central bank prospects, if not the cyclical outlook for the economy or the complex interplay between UK politics and Brexit. The BoE caught the market off-guard at its September MPR when it signaled its intention to commence tightening in ‘coming months’. The curve had assumed that the BoE would be on hold until early 2019. The result: a dramatic rate re-pricing -a November hike is now 75% priced and two full hikes are discounted by the end of 2018 -and a 5% short-covering scramble in GBP, its second-best monthly performance since 2009.

There are a number of challenges in translating a materially altered monetary landscape to GBP: There is still a lack of clarity as to what exactly has prompted the shift in the BoE’s reaction function as the MPC has offered partial and sometimes conflicting explanations for its abrupt change of heart.

Thus, a famous saying goes, never put all eggs into the single basket, we are currently running long GBP vol risk via a GBPCHF vs. EURCHF gamma spread where implied vols are well located near the bottom-end of a long-term range, the underlying spot prices are trading close to the middle of the recent 1.30-1.36 range. Our underlying bias is that the rebound from 1.30 is corrective for a move through 1.30 towards 1.28, potentially 1.25.

The vol spread has a desirable tendency for one-sided eruptions in favor of a wider GBPCHF premium during market crashes, enjoys a healthy positive carry at inception and is well-insulated from SNB shenanigans.

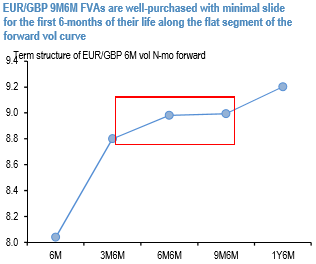

Given the timing unpredictability of twists and turns in the UK policy story, however, it is worth considering maturity diversification of a defensive GBP sleeve of trades via slightly longer-dated vol structures that also have the added advantage of slower decay than shorter-expiry options.

6M in 9M EURGBP forward volatility (9M6M FVAs) fits the bill, since it provides a 6-month runway of little/no static slide along a flat long-end vol curve (refer above chart), is marginally (0.5 vol) cheap on an RV basis versus equivalent GBPUSD structures, and has the additional kicker of participating in any Euro-related volatility brought about by either a more aggressive than expected ECB taper or resurgence of Italian election risk premium.