US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

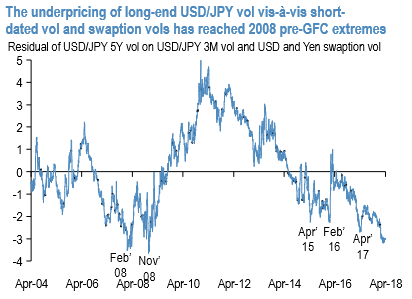

The lifelessness of FX vols this year in the face of stock market jitters and rise in interest rate volatility has surprised many including us, but at least some allowance can be made there for the unpredictability of contagion channels that transfer volatility from one asset to another.

One pocket of the FX vol market where it is difficult to offer even that token excuse because of the direct impact of interest rate volatility on options pricing is long-dated yen vol.

Regular readers will recall that we have been bullish long-end yen volatility for a good few months as a low bleed, good value all-weather portfolio hedge since 4Q’17, without any success so far it has to be admitted. USDJPY 5Y ATM vol is now nearly unchanged on the year after subsiding from its VIX shock highs, which does not sound like an acutely disappointing outcome till one granularly examines the mathematical building blocks of longer-dated FX vol: short-dated USDJPY vol as measured by 3M ATMs is up 0.3 % pts. YTD, an equally weighted blend of 1Y4Y, 2Y3Y, 3Y2Y and 4Y1Y US swaption vol is +10abp on the year, the corresponding Yen swaption vol is -2 abp and 3m realized correlation between USDJPY spot and (US-Japan) 5Y swap rate differential –the most crucial building block of long-dated vol pricing –has fallen a mammoth 30%-50% pts since the turn of the year.

The tiny drop in yen swaption vol aside, every single piece of the option pricing puzzle suggests long-end vols should have crept higher this year; that they have not leaves them screening as cheap relative to contemporaneous drivers as at their extreme in early 2008(3 vol pts. below model fair value – (refer 1st chart).

After the painful purge of vega longs towards the end of last year, we were cautious about further vol depressing flows coming online from Japanese importer hedging, which typically tend to cluster around March and April around the new Japanese fiscal year (refer 2nd chart). The bulk of the vol compression should now be behind us judging from this seasonal pattern, though the flow-driven cap on vol may remain in place through the end of the month if history is any guide. A leak lower in 5Y ATMs towards 9.0 or below from here should serve as decent entry points into strategic longs. Courtesy: JPM

Currency Strength Index: FxWirePro's hourly USD spot index has shown 50 (which is bullish), while hourly JPY spot index was at -83 (bearish) while articulating at 13:27 GMT. For more details on the index, please refer below weblink:

http://www.fxwirepro.com/currencyindex.

FxWirePro launches Absolute Return Managed Program. For more details, visit: