Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning

Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  ‘Vibe coding’ is fun and easy, but there’s a major catch

‘Vibe coding’ is fun and easy, but there’s a major catch  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning

BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning  Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate

Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

By the end of 2016, we expect USD/CNY to be testing 7.0 due to a mix of cyclical USD strength as well as domestic factors. FX intervention cannot continue indefinitely.

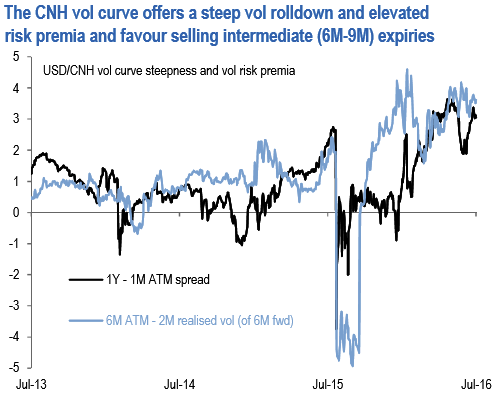

The orderly, low vol depreciation of the RMB has been one of the most noteworthy features of currency markets in recent months.

The credibility of the CFETS basket has dampened RMB volatility such that the tight correlation between spot direction and realized vol has broken down, with the latter clocking no higher than 3%4% despite June’s 2% USD/CNH rally spanning the Brexit discontinuity.

The steady depreciation of the CNY basket this year has reduced the odds of a large one-off devaluation that many market participants had feared, and tail risks of a repeat of August’2015/January 2016 have further fallen due to a combination of a more benign Fed outlook, a more advanced corporate deleveraging process for offshore borrowings and scope for bond inflows on the back of potential CGB inclusion in major bond indices.

CNY FX: Devaluation still in play but tail risks have fallen", this is suggestive of a contained realized CNH vol environment over the next few months, reinforced by the recovery in global risk appetite and PBoC's desire to ensure exchange rate stability ahead of key upcoming event risks (G20, SDR inclusion).

At a more tactical level, the pattern of fix management this week suggests that 6.80 may prove a sticky level for CNY in the short-term, which could induce a period of consolidation in what has been a near straight-line trend in Q2 and further soften delivered vol.

Short vol is, therefore, the appropriate stance in our view to collect the substantial risk premium built into option prices by way of implied vs. realized spreads and slide/rolldown along a steeply upward sloping vol curve.

As a result, we enter short 6M straddles in our FX portfolio model. Admittedly, absolute implied vol levels have seen a decent correction from their Q1 peak and perhaps have limited room for further declines such that instant P/L gratification from a vega re-mark lower is unlikely.

We view the 6M vol short as more of a patience trade anchored by PBoC policy to monetize vol curve steepness and anemic realized vol. For those who prefer to avoid uncapped short CNH option positions.

We recommend two alternatives: (a) overlay short option positions on long spot/forward positions in covered USD call constructs as a way of mitigating cost-of-carry on the former; and (b) buy6M 10D strangles as a tail hedge against straddle shorts given historically tight CNH flies (chart4). Investors not averse to exotic options can increase.