FxWirePro: EUR/ AUD neutral in the near term, scope further downside

FxWirePro: EUR/ AUD neutral in the near term, scope further downside  FxWirePro: AUD/USD eases as investors await U.S. employment figures

FxWirePro: AUD/USD eases as investors await U.S. employment figures  FxWirePro: GBP/USD rises as weak U.S. jobs data pressures dollar

FxWirePro: GBP/USD rises as weak U.S. jobs data pressures dollar  FxWirePro- Woodies pivot (Major)

FxWirePro- Woodies pivot (Major)  FxWirePro: GBP/AUD eases slightly, focus on near-term support

FxWirePro: GBP/AUD eases slightly, focus on near-term support  FxWirePro : USD/CAD falls as strong Canadian jobs data lifts loonie

FxWirePro : USD/CAD falls as strong Canadian jobs data lifts loonie  FxWirePro : EUR/NZD holding below 38.2% fibo ahead of US data

FxWirePro : EUR/NZD holding below 38.2% fibo ahead of US data  FxWirePro: USD/CNY slips as strong China exports data Lift yuan

FxWirePro: USD/CNY slips as strong China exports data Lift yuan  FxWirePro: GBP/AUD under pressure after disappointing U.S. employment data

FxWirePro: GBP/AUD under pressure after disappointing U.S. employment data  EUR/USD Rockets Past 1.1560 as Soft U.S. Jobs Data Fuel Fed Rate-Cut Surge

EUR/USD Rockets Past 1.1560 as Soft U.S. Jobs Data Fuel Fed Rate-Cut Surge  Major Pair Currency Score: NZD/USD and AUD/USD Lead Forex Rally with Perfect 100 Scores

Major Pair Currency Score: NZD/USD and AUD/USD Lead Forex Rally with Perfect 100 Scores  FxWirePro: EUR/AUD slips after surprise U.S. employment data

FxWirePro: EUR/AUD slips after surprise U.S. employment data  FxWirePro: NZD/USD retreats as Middle East instability weighs

FxWirePro: NZD/USD retreats as Middle East instability weighs  FxWirePro- Woodies pivot (Major)

FxWirePro- Woodies pivot (Major)  AUDJPY Bears Poised: Sell Rallies at 111.55 for 108 Target with 112.20 Stop

AUDJPY Bears Poised: Sell Rallies at 111.55 for 108 Target with 112.20 Stop  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary

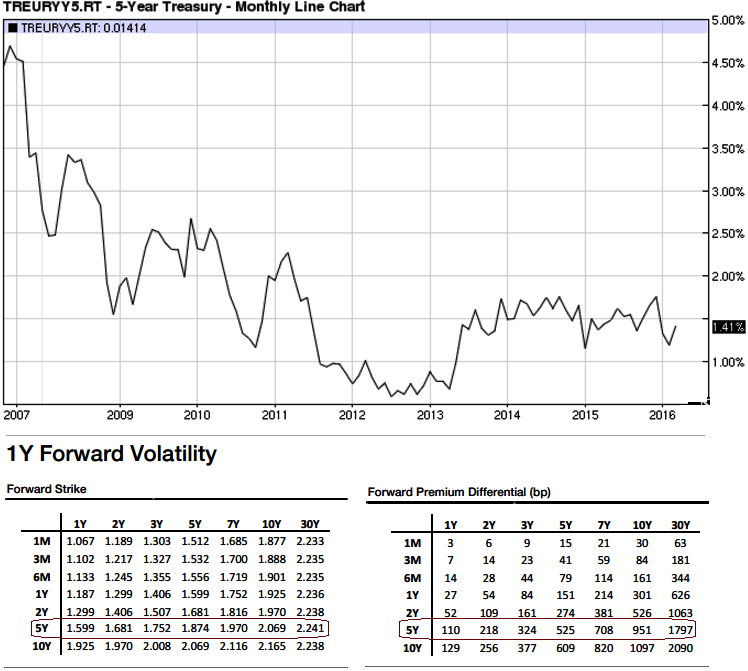

U.S.5Y treasury yield is flashing at 1.41% an increase from previous 1.38%, up about 2.61%.

14-day Real Strength - 55.11%

14-day Stochastic %K - 29.95%

14-day Stochastic %D - 35.61%

With 5yT yields down 15bp on the week, and 5s30s steepening by 8bp.

While WTI oscillating at $40 a barrel (3-months highs), and 5y breakevens continue to push higher into the 150 level. Expectations for the second hike were again pushed back to 2017.

On the grid, the left side led the underperformance on the dovish FOMC. Gamma was better offered with programme sellers hitting 1m-2m expiries, but pressure extending out to 6m.

With the FOMC meeting reinforcing the ranges, the bias near-term should be for lower volatility, Forward volatility (1y forward with vol triangles) Forward volatility continues to look slightly rich for short maturities, particularly on the left side of the grid, but elsewhere the grid looks cheap.

Hence, the recommendation goes this way, for long 1y forward 1y1y volatility (through a triangle go long in 2y1y and 1y1y straddles versus 1y2y straddles, equal notional, with strikes set to the 1y2y forward).