SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation

SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring

Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  World game at war: why some European nations have threatened a World Cup boycott

World game at war: why some European nations have threatened a World Cup boycott  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

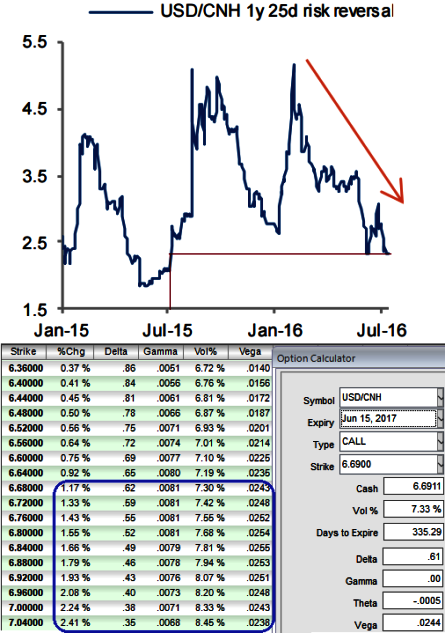

The Chinese economy grew 6.7% YoY in Q2 2016, unchanged from Q1, to bolster the growth in order to achieve 6.5-7.0% growth target, further monetary policy easing is still on the table. The slowdown in M2 growth in recent months hints that the PBoC has room to conduct monetary policy easing.

As stated in our recent write up on USDCNH IVs that shows the divergence with the realized volatility, shorting vega is advisable in such cases. Therefore, we call for below option strategy considering the on-going robust bullish environment last has lasted since 2014.

Buy USDCNH 1y Seagull strikes 6.55/6.85/7.20 Indicative offer: 0.42% (vs 0.82% for the call spread strikes 6.85/7.20, spot ref: 6.6910). This structure is a standard 1y call spread strikes 6.85/7.20 half financed by selling a put strike 6.55, offering beyond 7.20 a maximum leverage of 11x at the expiry.

With no digital risk involved and thanks to the limited convexity of long-dated options, the position can be conveniently delta-hedged if the spot moves lower in the early stages.

Risk reward profile: The 1y risk reversal is trading at a one-year low as shown in the diagram. It provides a good entry point to reload topside exposure despite the expensive volatility and also be noted that the healthy vega and gamma flashes on OTM call strikes. It also means that the vol market does not discount a disordered RMB depreciation, further supporting our short vega view.

Three-year-old depreciation trend reverses, the supply-demand imbalance in capital flows reaches equilibrium or hard-landing risks recede, causing the nearly three-year-old RMB depreciation cycle to reverse. The structure would face unlimited losses if USDCNH trades below the 6.55 strike in one year.

Vanilla calls or call spreads are too expensive when considering the probability-weighted terminal value of CNH a year from now. Under the premise that USDCNH only retraces a modest portion of the recent gains (similar to past experience when after an up move USDCNH did not revisit the lows and that there are no strong arguments for sustained appreciation on fundamental grounds, selling downside optionality can cheapen the cost of the call spread quite significantly.