With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer

Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum

Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

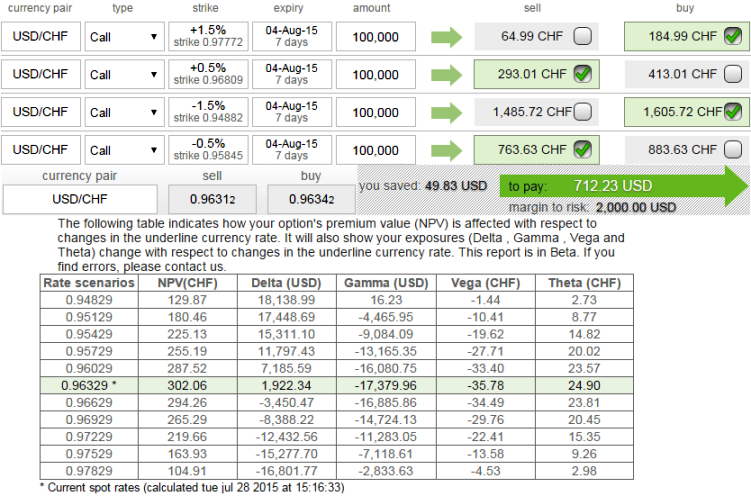

Since the implied volatility of USDCHF is perceived to be minimal, so here comes a multiple leg of option strategy for regular traders of this currency cross when there is little IV. A total of 4 legs are involved in the condor options strategy and a net debit is required to establish the position.

The trader can construct a long condor option spread as follows, as shown in the figure; the trader can implement this strategy using call options with similar maturities.

So strategy goes this way, writing 7D (-0.5%) In-The-Money call and buying deep striking (-1.5%) 0.84 delta In-The-Money call, writing a higher strike (0.5%) Out-Of-The-Money calls and buying another deep striking (1.5%) Out-Of-The-Money 0.17 delta call for a net debit.

Maximum returns for this strategy is achievable only when the exchange rate of USDCHF falls between the 2 middle strikes at maturity. It can be derived that the maximum profit is equal to the difference in strike price of the 2 lower striking calls less the initial debit taken to enter the trade.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: USDCHF low implied volatility portrays hedging with condor spreads

Tuesday, July 28, 2015 9:56 AM UTC

Editor's Picks

- Market Data

Most Popular