‘Vibe coding’ is fun and easy, but there’s a major catch

‘Vibe coding’ is fun and easy, but there’s a major catch  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform

How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data

CAD sharply depreciated by as much as 4.8% from mid-April highs on a layering of multiple concerns that suddenly gathered around Canada. These risks include fresh concerns over the US-Canada trade relationship, the potential for sharply lower oil prices, and the re-emergence of housing market related financial stability vulnerabilities.

While all of these developments could potentially impart a significant negative shock to the Canadian economy and thus the currency, none of these risks have been realized yet, nor are they necessarily acute.

The lumber tariff was mostly an idiosyncratic sideshow, and NAFTA renegotiation risks are still poorly defined and medium-term, not acute.

As we discussed in a recent note, Trump Trade Policy and Canada: Signal or Sideshow?, the US-Canada lumber dispute has been ongoing for decades, the US trade enforcement action should have been well anticipated, and therefore should not be read necessarily as a signal about how the broader US-Canada trade relationship will play out.

Instead, NAFTA uncertainty remains low-grade and medium-term (the administration has not even formally started the renegotiation process, which is awaiting the confirmation of the USTR).

Costless collars to hedge aggressive bullish outlook

The nutshell above explains that hedgers’ interests have been neutral but upside risks are lingering, however, no new shift in sentiments are observed. As a result, we don’t see much traction OTM calls.

More broadly, with the post-referendum upsurge in uncertainty proving short-lived, the main drag on the economy is now expected to come through the hit to consumer purchasing power resulting from the weakness of sterling, with the bulk of the impact due to take effect in 2017.

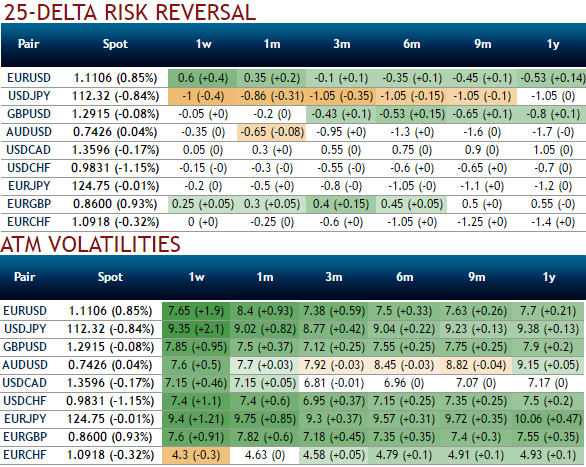

In the recent times, CAD vols skews destabilized too much especially on crude’s price sustainability, while USD volatility market normalized sharply (you could be observed that in USDCAD IV skews) which has been well balanced on both the sides. The liquidity recovered and the extreme positioning was ultimately absorbed. The price action is not taking the direction of an imminent new trend. As a result, the options market aggressively unwound smile positions.

Contemplating major trend and short-term upswings, anyone who wishes to carry long USDCAD exposures, a collar options trading strategy is recommended. This could be constructed by holding the total number of units of the underlying spot FX while simultaneously buying a protective put and shorting call option against that holding. The puts and the calls are both OTM options having the same expiration month and must be equal in the number of contracts.

The collar is a good strategy to use if the options trader is writing covered calls to earn premiums but wish to protect himself from an unexpected sharp drop in the price of the underlying security.