BOJ Holds Rates at 1% as Inflation Outlook Eases, October Rate Hike Still Possible

BOJ Holds Rates at 1% as Inflation Outlook Eases, October Rate Hike Still Possible  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields

Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields  RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist

RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring

Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics

Although the US dollar appears to be in a slightly stronger position, it’s not convincing, an interesting change as USDJPY seemed to move in one direction only recently: to the downside. Nevertheless, we can’t find a game changer for the dollar anywhere. Yes, the White House has agreed a new economic packet with the Republicans in the Senate, but it does not contain any major surprises. And it seems nearly utopian to expect that a compromise can be reached with the Democrats by the end of the month when important aid measures from the last packet start expiring. The Democrats had demanded much further reaching support measures. Many Americans are therefore facing a tough start into August.

As a result, the Fed decision tomorrow is centre stage. Before the blackout period (when Fed members no longer comment on monetary policy in the run up to a meeting) the Fed central bankers had sounded increasingly cautious. This was mainly due to rising infection numbers which threaten to halt the economic recovery in the US. Even if tomorrow is unlikely to be the right moment for a more expansionary monetary policy approach, the Fed will no doubt sound prepared for further easing. That is likely to limit the upside in USDJPY.

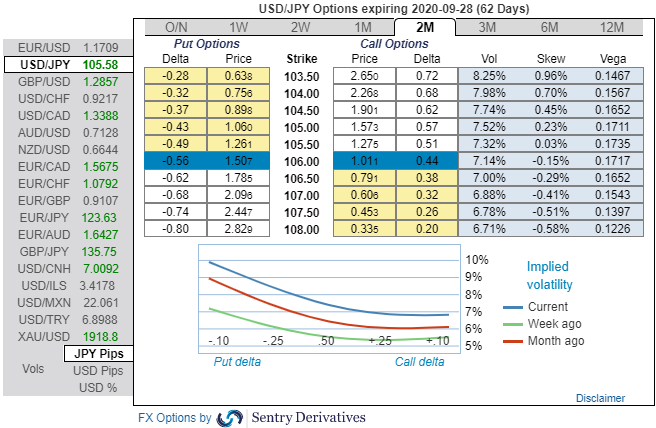

While our perspectives on Japanese yen against the dollar remains towards 100 levels. If not for liquidity constrains a contained yen upside could be efficiently expressed via defensive USDJPY OTM put calendars that utilize the once in a generation skew-vol setup.

We opt for fading the curve inversion via vanillas on the weak side of the riskies to avoid left tail exposure.

At spot reference: 105.608 levels, we advocate buying a 2M/2w 106.500/102 put spread (vols 8.25 vs 7.14 choice), we would like to maintain the ITM long leg with the diagonal tenors on hedging grounds.

The rationale: The positively skewed IVs of 2m tenors of USDJPY contracts are still signifying the hedging interests for the bearish risks. We see bids for OTM strikes up to 103.50 levels (refer 1st nutshell), whereas 2w skews signal both bullish and bearish risks.

To substantiate this directional stance, one can trace out fresh bids of positive numbers for the existing bearish risk reversal numbers, this also signals current hedging interests for the downside risks amid mild upswings (2nd nutshell).

Alternatively, shorting USDJPY futures contracts of mid-month tenors have been advocated, on hedging grounds, we upheld the same positions, as the underlying spot FX likely to target southwards in the medium run. Courtesy: Sentry, Saxo & Commerzbank