US Launches New Iran Strikes as Strait of Hormuz Conflict Escalates, Oil Prices Rise

US Launches New Iran Strikes as Strait of Hormuz Conflict Escalates, Oil Prices Rise  Japan Regional Bank Stocks Drop After Zentoshin Bankruptcy Sparks Credit Risk Concerns

Japan Regional Bank Stocks Drop After Zentoshin Bankruptcy Sparks Credit Risk Concerns  South Korea’s KOSPI Plunges as Samsung, AI Chip Stocks Trigger Market Sell-Off

South Korea’s KOSPI Plunges as Samsung, AI Chip Stocks Trigger Market Sell-Off  FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022  Bernstein Raises 2026 Nickel Price Forecast as Indonesia Tightens Supply

Bernstein Raises 2026 Nickel Price Forecast as Indonesia Tightens Supply  Asian Currencies Slip as Stronger US Dollar, Iran Tensions Pressure Regional FX

Asian Currencies Slip as Stronger US Dollar, Iran Tensions Pressure Regional FX  Nasdaq Futures Slide as AI Chip Stocks Sink Despite Samsung Earnings; SpaceX Debuts in Nasdaq-100

Nasdaq Futures Slide as AI Chip Stocks Sink Despite Samsung Earnings; SpaceX Debuts in Nasdaq-100  US Stock Futures Steady as US-Iran Tensions and Fed Inflation Concerns Weigh on Markets

US Stock Futures Steady as US-Iran Tensions and Fed Inflation Concerns Weigh on Markets  Venezuela Earthquake Death Toll Climbs to 3,811 as Government Seeks Sanctions Relief

Venezuela Earthquake Death Toll Climbs to 3,811 as Government Seeks Sanctions Relief

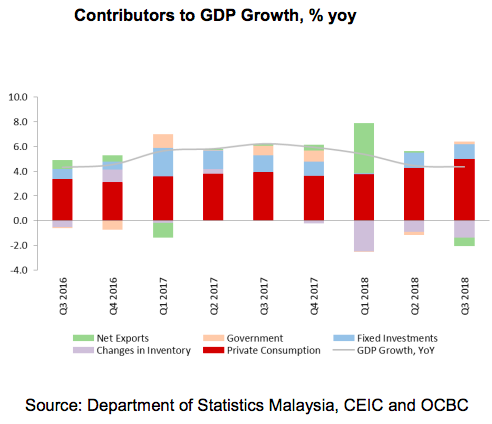

Malaysia’s economic growth for the fourth quarter of this year is expected to come in at 4.2 percent y/y, while the full-year expansion is seen at 4.6 percent y/y, according to the latest research report from OCBC Bank.

GDP growth slowed further for Q3 2018 at 4.4 percent y/y, vs 4.5 percent y/y in the Q2 as the mining and quarrying sector continued to struggle whilst private consumption surged. The growth this quarter is the slowest it has been since the Q3 2016 when the economy grew at 4.3 percent y/y.

Private consumption as usual was the biggest contributor to growth followed on by fixed investment. Government consumption expanded positively this time around but net exports saw a decline.

There were still weaknesses in the commodities sector for the quarter. The mining and quarrying sector continuing to struggle as it further declined by 4.6 percent y/y, vs Q2 at -2.2 percent y/y. Production of crude oil & condensate and natural gas continued. The agricultural sector also saw a decline of 1.4 percent y/y but this decrease was lower than the prior quarter at -2.5 percent y/y.

However, the palm oil sector continued to see weaknesses. The central bank had already earlier warned in their November monetary policy statement of “prolonged weakness in the mining and agriculture sectors”.

Net exports declined this quarter by 7.5 percent y/y (Q2 2018: 1.7 percent y/y) as exports declined by 0.8 percent y/y (Q2 2018: 2.0 percent y/y). This occurred as commodities exports continued to see a contraction albeit smaller at 3.0 percent y/y (Q2 2018: -3.8 percent y/y). Crude palm oil exports continued to decline whist growth in exports of mineral resources, particularly in crude petroleum improved.

However, non E&E exports particularly in petroleum products did moderate. Further, the silver lining for the quarter is that growth of gross fixed capital formation actually accelerated to 3.2 percent y/y (Q2 2018: 2.2 percent y/y).

Furthermore, this growth was driven by private sector investment which continued to grow strongly at 6.9 percent y/y whilst public sector investment continued to decline by 5.5 percent y/y.

"For the final quarter, we are now expecting growth to moderate to 4.2 percent y/y which means we forecast the entire year growth to come out at 4.6 percent y/y. The main driver of this slowdown would obviously be that we foresee private consumption growth slowing down significantly as the tax holiday comes to an end and consumers had frontloaded expenditure in the previous quarter. Exports will probably see some recovery although not significantly whilst investment growth should still continue to exhibit some strength," the bank commented.