German Industry Employment Falls to Lowest Level in a Decade

German Industry Employment Falls to Lowest Level in a Decade  Japan Signals Readiness to Intervene as USD/JPY Nears 161 Amid Yen Weakness

Japan Signals Readiness to Intervene as USD/JPY Nears 161 Amid Yen Weakness  Oil Prices Ease as Markets Weigh U.S.-Iran Peace Deal and Strait of Hormuz Reopening

Oil Prices Ease as Markets Weigh U.S.-Iran Peace Deal and Strait of Hormuz Reopening  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Yen Near 40-Year Lows Despite BOJ Rate Hike, Markets Brace for Possible Intervention

Yen Near 40-Year Lows Despite BOJ Rate Hike, Markets Brace for Possible Intervention  Trump Questions USMCA Renewal as Trade Talks Continue

Trump Questions USMCA Renewal as Trade Talks Continue  Asian Currencies Steady as Dollar Holds Firm Ahead of Fed Decision and US-Iran Deal Details

Asian Currencies Steady as Dollar Holds Firm Ahead of Fed Decision and US-Iran Deal Details  ASX Proposes New Share Dilution Limits for Public Takeovers

ASX Proposes New Share Dilution Limits for Public Takeovers  US Stock Futures Jump on Reports of Preliminary US-Iran Peace Deal Despite Fed’s Hawkish Outlook

US Stock Futures Jump on Reports of Preliminary US-Iran Peace Deal Despite Fed’s Hawkish Outlook  Australia Eases Capital Gains Tax Reforms to Support Small Businesses and Startups

Australia Eases Capital Gains Tax Reforms to Support Small Businesses and Startups  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  Gold Prices Rebound on U.S.-Iran Peace Deal Optimism Despite Fed Rate Hike Signals

Gold Prices Rebound on U.S.-Iran Peace Deal Optimism Despite Fed Rate Hike Signals

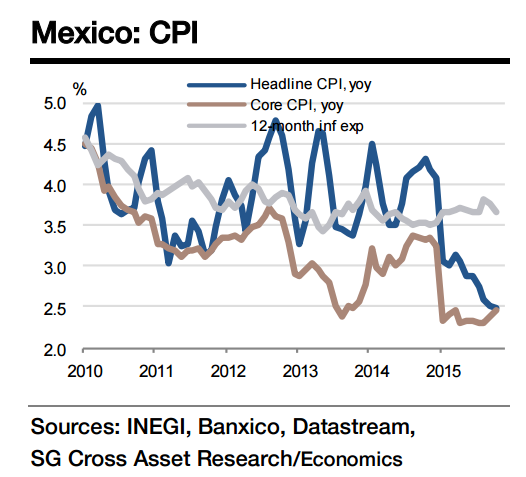

While the headline inflation rate has slipped further over the past couple of months, core inflation has moved up from 2.3% yoy in August to 2.47% yoy in October on the back of a rise in inflation in categories such as health and personal care, apparel, and furniture and domestic accessories.

Also, dwelling inflation - the key factor behind the sharp decline in inflation earlier this year - has moved up to 0.58% yoy from 0.45%. Mid-month inflation is expected to moderate to 2.47% yoy in November. In sum, core inflation has remained low, while stabilising or even rising, and the weakness in the headline inflation has been driven primarily by the food and transport segments. October and November data should hint that the deceleration (and critically, food inflation) is in last leg and that we will see it move above Banxico's target in January 2016.

Inflation should revert to its medium-term trend in 2016 when the base effect of lower telecom and energy prices ebbs. Essentially, the inflation situation remains conducive to Banxico's current accommodative stance, and growth and the Fed's stance are likely to be the key factors in monetary policy decisions over the next couple of quarters.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Mexico inflation remains low on food and transport prices; core inflation rising

Tuesday, November 24, 2015 12:32 AM UTC

Editor's Picks

- Market Data

Most Popular