SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer

Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns

Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns  Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum

Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum  Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

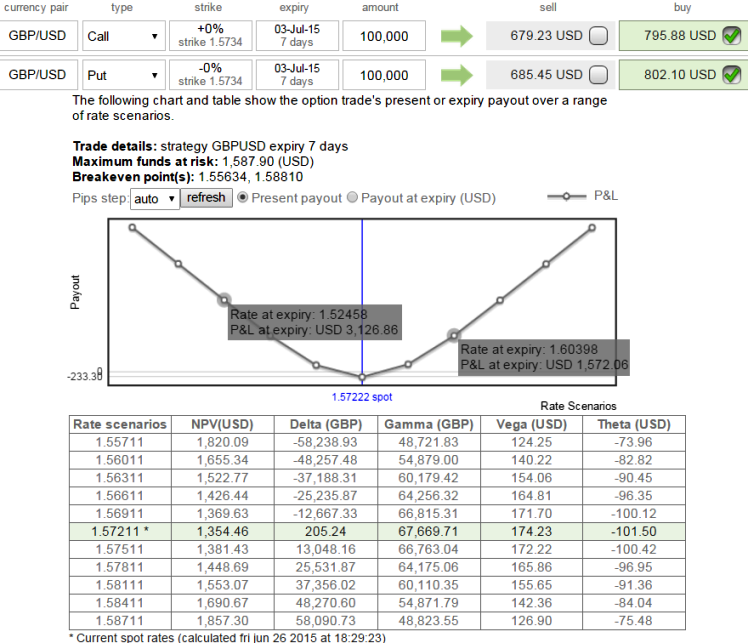

The portfolio contains an ATM call and ATM put of the same maturity of same underlying currency then they must have the same present value.

Else, arbitrager can add longs on the undervalued portfolio and short on overvalued portfolio to make a risk free profit on expiration day.

Hence, taking the need to calculate the present value of the cash component into account using a suitable risk-free interest rate, we have computed and illustrated the Put call parity of GBP/USD straddle:

We considered At-The-Money options while calculating Put call parity of GBP straddle structure as shown in the figure.

C = S + p - Xe-r (T- t)

= 1.5725 + 802.06 - Euler (1.5725*2.71828) - 0.02*(7)

= 799.218

P = c - S + Xe-r (T- t)

= 795.86 - 1.5725 + Euler (1.5725*2.71828) - 0.02*(7)

= 798.422

Where,

S = Current Exchange Rate at around 1.5725

X = Exercise price (strike) of option = 1.5725

C = Call Value = 795.86

P = Put price = 802.06

e = Euler's constant - approximately 2.71828 (exponential function on a financial calculator)

r = continuously compounded risk free interest rate is deemed as 2%

T-t = term to expiration measured in years = 7 days

T = Expiration date

t = Current value date

Inference: Before jumping into a conclusion of above calculations, one has to be mindful of how the supply and demand impacts option prices and how all option values (at all the available strikes and expirations) on the same underlying exchange rates are related.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Put call parity of GBP/USD straddles

Friday, June 26, 2015 1:10 PM UTC

Editor's Picks

- Market Data

Most Popular