US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

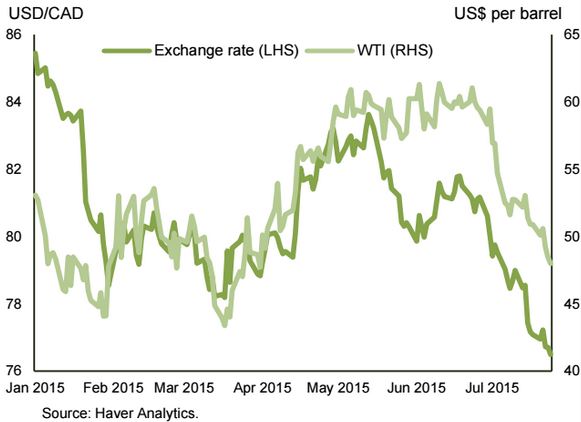

A variety of factors conspired to take the price of WTI below US$50 per barrel this week for the first time since March. When combined with last week’s Bank of Canada interest rate cut, this pushed the loonie under 77 US cents for the first time in over a decade.

Helping to round out some of the details on May’s economic performance, retail and wholesale trade data have reinforced our view that real GDP will be essentially flat in the month.

Add it all up and we are tracking a second quarterly contraction in real GDP in Q2 of roughly 1.0% (annualized). Looking beyond Q2, the lower Canadian dollar and interest rates should be supportive of growth, although the continued weakness in oil prices may delay renewed investment in the energy sector.

But looking beyond the second quarter, the lower Canadian dollar and lower interest rates bode well for Canadian exporters and manufacturers. Consumers should also to benefit. However, if current trends in commodity prices continue, business investment, particularly in the energy sector, may be slow to ramp up. The housing sector is likely to remain a bright spot in 2015, but can be expected to cool next year as affordability continues to erode on the back of national home price growth that is outpacing income growth. And with 5-year Government of Canada bond yields at around 80 bps, it’s hard to imagine rates going much lower.