Trump and Iran Sign Framework Peace Deal in France Amid Ongoing Middle East Tensions

Trump and Iran Sign Framework Peace Deal in France Amid Ongoing Middle East Tensions  German Industry Employment Falls to Lowest Level in a Decade

German Industry Employment Falls to Lowest Level in a Decade  Oil Prices Slide as U.S.-Iran Deal and Hormuz Reopening Ease Supply Concerns

Oil Prices Slide as U.S.-Iran Deal and Hormuz Reopening Ease Supply Concerns  US Stock Futures Jump on Reports of Preliminary US-Iran Peace Deal Despite Fed’s Hawkish Outlook

US Stock Futures Jump on Reports of Preliminary US-Iran Peace Deal Despite Fed’s Hawkish Outlook  Asian Currencies Stabilize as Dollar Holds Near Two-Month High After Fed Hawkish Signal

Asian Currencies Stabilize as Dollar Holds Near Two-Month High After Fed Hawkish Signal  Oil Prices Steady as U.S.-Iran Truce Uncertainty and Middle East Tensions Keep Markets on Edge

Oil Prices Steady as U.S.-Iran Truce Uncertainty and Middle East Tensions Keep Markets on Edge  Dollar Hits One-Month High as Hawkish Fed Outlook Boosts Greenback

Dollar Hits One-Month High as Hawkish Fed Outlook Boosts Greenback

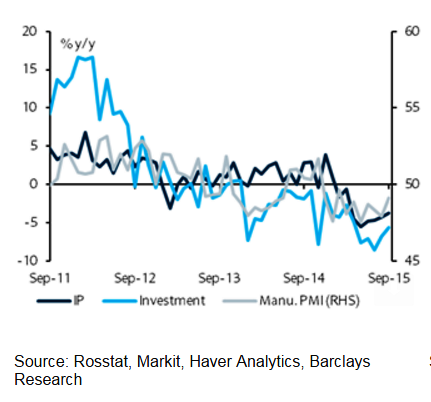

Russia's September real sector indicators provide some encouragement. Production indicators signal that the decline may have hit bottom and production is no longer declining. However, household consumption indicators imply further downside risks.

On the optimistic side, the decline in industrial production lessened to -3.7% y/y. This was the fourth monthly improvement from the nadir in May of -5.5% y/y. In addition, the seasonally adjusted index has improved off recent lows.

"This suggests that the industrial production decline has abated and there may be no further drop, although it is too soon to conclude that industrial production is ready to start increasing. Investment also appears to have turned the corner: improving for the second month to -5.6% y/y from the low of -8.5% in July", says Barclays.

Manufacturing PMI improved in September to 49.1, near the neutral level. Finally, unemployment fell to 5.2% from 5.3%. This is a reasonably uniform picture that the declines have ceased.

On the pessimistic side, indicators imply that household spending may fall further. Retail sales deteriorated to -10.4% y/y in September, considerably worse than last month and expectations, indicating that further declines in consumption are likely.

Real wages remained in deep decline, falling -9.7% y/y in September, only slightly better than the previous month. However, unemployment unexpectedly declined in September to 5.2% implying that employers are keeping wages low instead of laying off workers. It is possible that cutting employment will come later in the cycle if output levels remain depressed for an extended period.

"Overall, these indicators are interpreted to imply that the economy is near the bottom of its cycle and that the recession will not deepen much further. However, they provide no indication of a speedy recovery. A gradual L-shaped recovery is more likely from this recession as opposed to the previous V-shaped recoveries that Russia enjoyed in 1999 and 2009", added Barclays.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Russia's economy likely near bottom of the cycle

Tuesday, October 20, 2015 4:31 AM UTC

Editor's Picks

- Market Data

Most Popular