Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates  BOJ Rate Hike Expectations Rise Ahead of September Meeting

BOJ Rate Hike Expectations Rise Ahead of September Meeting  How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform

How an OpenAI safety test became a real-world cyberattack on the Hugging Face platform  Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war  Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

The Fed is likely to tighten monetary policy only by as much as markets allow without major turmoil. The Fed will try to avoid any further asset price inflation and ease any bubbles that have already emerged, such as in the sovereign bond market. During the 2004-07 period, when the Fed continuously tightened monetary policy, bond yields did not react and the housing bubble continued to expand.

With the U.S. expansion in its seventh year, the lack of price pressures is starting to raise deeper questions about whether the economy will produce the kind of demand that can get inflation to Fed's 2 percent goal. Based on the difference in yields between TIPS and nominal Treasuries, the 30-year inflation outlook fell to an annual rate of 1.49 percent last month -- the lowest since early 2009.

Various FOMC members have said that the Fed needs to avoid a repetition of the 2004-07 period. The Fed is likely of the opinion that the US consumer no longer needs a positive wealth effect to sustain consumption growth, given almost full employment, the likelihood of upcoming wage growth and the relief from the lower oil price. The Fed's bond purchases have effectively transferred some of the asset price appreciation related to the economic cycle towards an earlier stage of the cycle, helping the consumer to digest the debt/housing market overhang from the financial crisis.

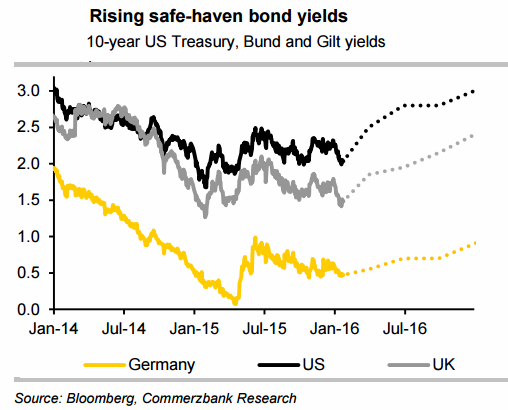

"Against this backdrop the Fed should succeed in gradually letting the air out of the bond bubble, and safe-haven bond yields are set to gradually increase. The rising relative attractiveness of sovereign bonds and the unwinding of the 'hunt-for-yield' should weigh on the returns of other asset classes resulting in years of asset price disinflation at the global level," said Commerzbank in a research note.

Besides rate hikes, the Fed has many tools to steer the process. Their bond holdings can be used to manage US Treasury yields. The policy spectrum ranges from the current reinvestment of any proceeds from their bond holdings, with the option of only partly reinvesting maturing debt or not at all, to outright bond sales. Data shows the amount of maturing US Treasury bonds in the Fed's System Open Market Account averages roughly USD22bn per month between 2016 and 2021.

U.S. Treasury yields fell to four-month lows on Friday after BoJ surprised investors by introducing negative interest rates in a further effort to stimulate the country's flagging economy. U.S. 10-Year Treasuries yield stood at 1.915 percent on the day, while 2-year yield dropped to a 3-month low of 0.766 percent on Friday before bouncing to 0.779 percent.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Safe-haven bond yields to gradually rise as Fed aims to ease bubbles in the sovereign bond market

Monday, February 1, 2016 11:25 AM UTC

Editor's Picks

- Market Data

Most Popular