Trump and Iran Sign Framework Peace Deal in France Amid Ongoing Middle East Tensions

Trump and Iran Sign Framework Peace Deal in France Amid Ongoing Middle East Tensions  Oil Prices Ease as Markets Weigh U.S.-Iran Peace Deal and Strait of Hormuz Reopening

Oil Prices Ease as Markets Weigh U.S.-Iran Peace Deal and Strait of Hormuz Reopening  Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX  German Industry Employment Falls to Lowest Level in a Decade

German Industry Employment Falls to Lowest Level in a Decade  Yen Near 40-Year Lows Despite BOJ Rate Hike, Markets Brace for Possible Intervention

Yen Near 40-Year Lows Despite BOJ Rate Hike, Markets Brace for Possible Intervention  Japan Signals Readiness to Intervene as USD/JPY Nears 161 Amid Yen Weakness

Japan Signals Readiness to Intervene as USD/JPY Nears 161 Amid Yen Weakness  Australia Eases Capital Gains Tax Reforms to Support Small Businesses and Startups

Australia Eases Capital Gains Tax Reforms to Support Small Businesses and Startups  Gold Prices Slide as Hawkish Fed and Strong Dollar Weigh on Bullion

Gold Prices Slide as Hawkish Fed and Strong Dollar Weigh on Bullion  Canada, British Columbia Launch $5 Billion Infrastructure Partnership to Boost Housing, Transit, and Healthcare

Canada, British Columbia Launch $5 Billion Infrastructure Partnership to Boost Housing, Transit, and Healthcare  Japan Inflation Stays Below BOJ Target Despite Rate Hike and Rising Energy Cost Risks

Japan Inflation Stays Below BOJ Target Despite Rate Hike and Rising Energy Cost Risks

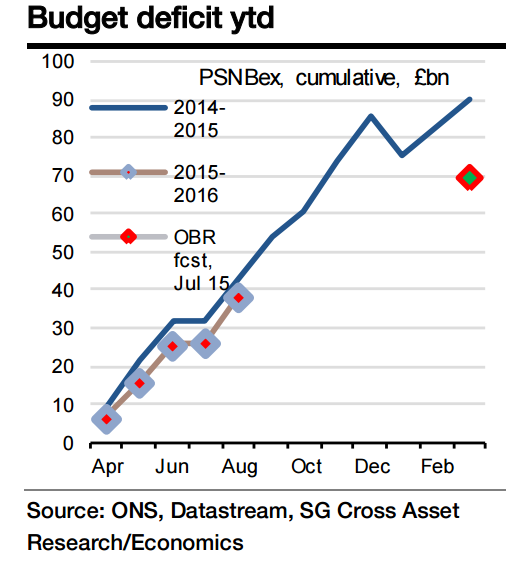

The monthly evolution of the budget deficit is highly erratic. In the first three months of the fiscal year, the PSNBex measure fell by a total of £6bn compared to a year earlier but then in the following two months was £1.6bn worse. So the year-to-date (August) improvement is £4.4bn. However, for the OBR projections for the full year to be met, the improvement would have to have been twice that.

The quality of the data on some of the key inputs is poor until quite late in the year so we should not be surprised at this volatility. Moreover, this also means that we should be cautious in interpreting the year-to-date performance as implying that the full year projection will be missed.

"For September we predict that the deficit will be the same as a year earlier at £11.0bn," notes Societe Generale.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

UK public finances improvement to stall temporarily in September

Monday, October 19, 2015 8:54 PM UTC

Editor's Picks

- Market Data

Most Popular