Dollar Eases as Middle East Conflict, Fed Outlook and Japan Pension Policy Drive FX Markets

Dollar Eases as Middle East Conflict, Fed Outlook and Japan Pension Policy Drive FX Markets  Goldman Sees Foreign Investors Driving India Stock Market Recovery

Goldman Sees Foreign Investors Driving India Stock Market Recovery  Asian Currencies Stay Rangebound as Middle East Tensions, Weak China GDP Weigh on Sentiment

Asian Currencies Stay Rangebound as Middle East Tensions, Weak China GDP Weigh on Sentiment  Asian Stocks Slide as Oil Surge, U.S.-Iran Tensions and Fed Rate Bets Weigh on Markets

Asian Stocks Slide as Oil Surge, U.S.-Iran Tensions and Fed Rate Bets Weigh on Markets  Asia Stocks Slip as Iran-Hormuz Tensions Lift Oil Prices, Dollar and Bond Yields

Asia Stocks Slip as Iran-Hormuz Tensions Lift Oil Prices, Dollar and Bond Yields  Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX  Iraq PM Visits Washington as U.S. Oil, Gas Deals Take Center Stage

Iraq PM Visits Washington as U.S. Oil, Gas Deals Take Center Stage

Headwinds to U.S. growth emanating from the soft global economic backdrop and elevated greenback were one of the motivations behind the Fed's decision not to raise rates in September. As we kick off October, these risks continue to loom and were highly apparent in this week's trade, manufacturing and employment data.

The advance report on U.S. international trade in goods - the new monthly indicator released on Tuesday - showed a dramatic deterioration in the merchandise trade balance in August, with the deficit widening from $59.1B to $67.2B. A combination of the strong dollar and subdued global demand weighed on exports, which fell by 3.5% m/m, marking the biggest decline since January. Meanwhile, imports gained 1.8% m/m, underscoring a comparatively robust level of domestic demand. While trade data will likely perform better next month, the extent of deterioration in the trade deficit in August suggests that the external sector will be a major drag on the U.S. growth in the third quarter.

The somber outlook for the global economy was reiterated this week, with the head of the IMF, Christine Lagarde, warning on Wednesday that global growth remains "disappointing and uneven". Global manufacturing activity largely reflected this assessment. Softness in PMI indicators across several economies increased the likelihood that the global economy could weaken further. India's manufacturing PMI hit a seven-month low in September, while those of South Korea and China remained stuck in contractionary territory. Eurozone manufacturing activity continued to expand; however, the PMI index slipped lower by 0.3 points, indicating a slightly slower pace of expansion.

Similarly, the U.S. ISM manufacturing index also fell, declining by 0.9 points to 50.2 in September and narrowly avoiding slipping into contractionary territory. The weakness was broad-based, with most sub-components and industries faring worse. However, perhaps most disconcerting was the deterioration in the forward-looking indicators suggesting that activity will likely remain subdued in the months ahead.

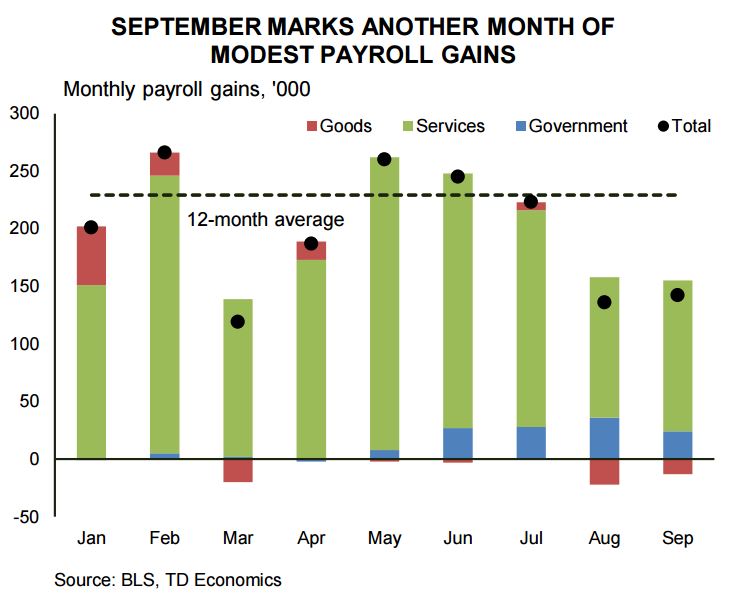

The trail of the global slowdown was also evident in September's non-farm payrolls, which rose by just 142k - the slowest pace of job creation since March. Manufacturing employment fell for a second consecutive month, while mining employment contracted for the ninth straight month. While the brunt of the losses was concentrated in these externally exposed industries, service sectors employment growth also softened to 131k from the 205k average over the last twelve months. Market reaction was swift, with 10-year Treasury yields falling by 18 basis points and expectations of the Fed hike being pushed to March.

The knee-jerk market reaction seems to be overdone. The slowdown in job creation cannot be chalked up to external factors exclusively. As the jobless rate is already beginning to approach its long-term trend level, job creation should naturally decelerate from its previous above-trend pace. It is worth noting that age-specific participation rates have remained relatively stable. With population aging, trend labor force growth is expected to be only about 80k a month. As a result, future expectations about job growth should reflect these factors.

Despite the looming global risks and slowing employment gains, the story remains positive for domestically-oriented sectors due to rising employment, low gasoline prices and improving real income.

Consumer confidence and spending continued to make strides over the last two months, both outstripping market. Ditto for light vehicle sales, which surged to 18.06 million in September - the highest pace of sales since 2005. Tailwinds from rising employment and incomes will continue to shore up consumer confidence and spending, with the latter poised to sustain an above-3% pace through the rest of the year.