Goldman Sachs Sees U.S. Dollar Holding Firm as Strong Economic Data Supports Outlook

Goldman Sachs Sees U.S. Dollar Holding Firm as Strong Economic Data Supports Outlook  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  J.P. Morgan Sees Major Upside for Prysmian as Optical Fiber Prices Surge

J.P. Morgan Sees Major Upside for Prysmian as Optical Fiber Prices Surge  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch

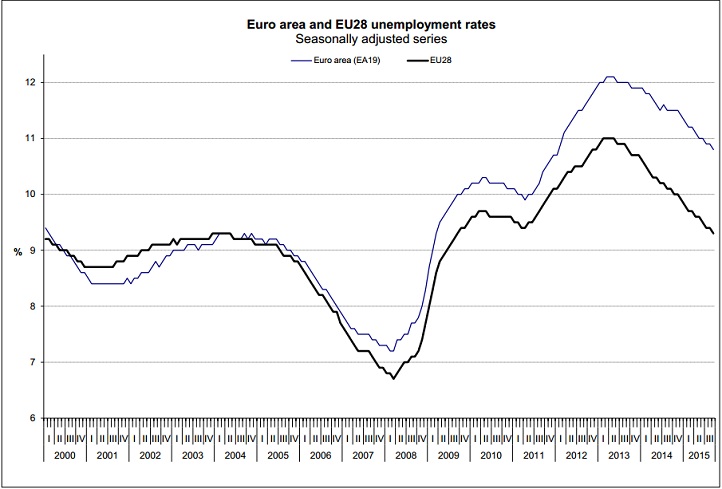

Euro zone unemployment rate dropped to 10.8% in September from 11% a month back. I have been arguing for further ECB action for quite some time, hints of which finally came at last meeting. And key corner piece of my argument has been fragmentation in employment and overall high level of it.

Unlike FED, employment is not a mandate of European Central Bank (ECB) but any sustainable demand driven inflation is not possible to achieve when a large chunk of the workforce doesn't have jobs.

Latest report shows that asset purchase is working with unemployment dropping fast but still not fast enough given the size of the workforce which runs in several millions sitting outside for so long.

ECB sure has the ability to do more given relatively smaller balance sheet size (in value and both % GDP) and inflation relatively low.

Regional employment growth review -

- Fragmentation is diminishing but still at the higher end. While unemployment rate at very low in Germany (4.5%), Malta (5.1%), Austria (5.7%), countries like Greece (25%), Span (21.6%), Cyprus (15.1%) suffering high level of unemployment.

- Moreover for most economies, level of unemployment is quite high - Portugal (12.2%), Italy (11.8%), France (10.7%).

Though Euro zone employment and growth, both headed in right direction, it remains too fragile to withstand headwinds from slowdown in China and debt crisis across emerging markets.

European Central Bank has made the right choice making it my favorite central bank and President Draghi an excellent orator.