Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum

Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum  Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies  Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer

Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

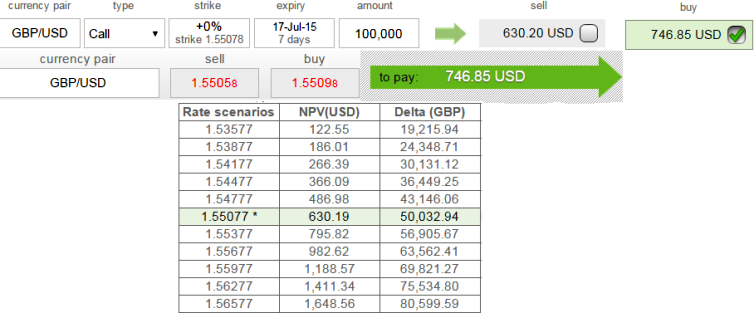

Delta signifies the equivalent FX spot outrights of a given position. This is the sensitivity of a position's value with respect to the spot rate.

This is useful to monitor directional risks so you may know how much your option's value will increase or diminish as the underlying market moves.

A higher delta value is desirable for an option holder, whilst a delta close to zero is desirable for the option writer; a buyer wants their option to become more valuable whilst a seller wants the option to become less valuable.

For an instance, as we can see in the chart that overall position in GBPUSD behaves as if it was long 50,032.94 GBPUSD spot.

But in real terms, if at all GBPUSD spot were to move up by one pip then the relative sensitivity in option premium would be USD 0.5003. To hedge a call, one would invest the option price proceeds into Δt∗St+Bt=ct (where Δ=delta).

These terms may seem quite strange to you but nothing rocket science hidden in it, we would run you through these blackscholes in upcoming articles.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Why delta is crucial in option strategy

Friday, July 10, 2015 1:59 PM UTC

Editor's Picks

- Market Data

Most Popular