U.S. Stock Futures Slide as Tech Rout Deepens on Amazon Capex Shock

U.S. Stock Futures Slide as Tech Rout Deepens on Amazon Capex Shock  Gold and Silver Prices Slide as Dollar Strength and Easing Tensions Weigh on Metals

Gold and Silver Prices Slide as Dollar Strength and Easing Tensions Weigh on Metals  Global Markets Slide as AI, Crypto, and Precious Metals Face Heightened Volatility

Global Markets Slide as AI, Crypto, and Precious Metals Face Heightened Volatility  Australian Household Spending Dips in December as RBA Tightens Policy

Australian Household Spending Dips in December as RBA Tightens Policy  Nikkei 225 Hits Record High Above 56,000 After Japan Election Boosts Market Confidence

Nikkei 225 Hits Record High Above 56,000 After Japan Election Boosts Market Confidence  Trump Lifts 25% Tariff on Indian Goods in Strategic U.S.–India Trade and Energy Deal

Trump Lifts 25% Tariff on Indian Goods in Strategic U.S.–India Trade and Energy Deal  U.S.-India Trade Framework Signals Major Shift in Tariffs, Energy, and Supply Chains

U.S.-India Trade Framework Signals Major Shift in Tariffs, Energy, and Supply Chains  Bank of Japan Signals Readiness for Near-Term Rate Hike as Inflation Nears Target

Bank of Japan Signals Readiness for Near-Term Rate Hike as Inflation Nears Target

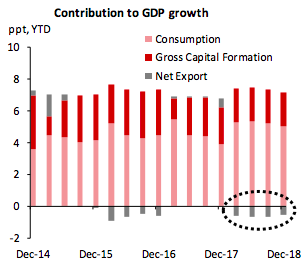

China’s real GDP growth fell further to 6.4 percent y/y in 4Q18 from 6.5 percent in 3Q18 as expected. Net export continued to drag the overall performance for the fourth straight quarter in spite of slumping oil price.

This largely mirrored the negative export growth in December after front-loading activities ended. The monthly data pointed to a grim outlook for 1Q19. Retail sales inched up to 8.2 percent y/y in December from 8.1 percent in November, staying at the lowest range since 1999.

Expenditure on most other discretionary goods such as cosmetics, jewellery, and automobile remained weak. Obviously, consumer confidence has been sapped by job insecurity and slower wage growth.

Fading credit impulse on the back of regulation tightening points to further weakness ahead. Infrastructure investment was a bright spot; growth was positive for a second consecutive month (5.7 percent in December vs 2.5 percent in November (3mma)).

The National Development and Reform Commission (NDRC) greenlighted RMB1.2 billion worth of infrastructure projects in 4Q18, the highest in three years.

"We expect the quota of special bond issuance (excluded from official budgets) to increase to RMB2 trillion in 2019 from RMB1.35 trillion last year. Off-budget expansions will likely include the re-launching of special construction fund," DBS Research commented.