RBI Hits Pause as Geopolitical Storm Clouds Gather

RBI Hits Pause as Geopolitical Storm Clouds Gather  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  Jerome Powell Warns Against Politicizing the Federal Reserve, Defends Democratic Institutions

Jerome Powell Warns Against Politicizing the Federal Reserve, Defends Democratic Institutions  BOJ Raises Interest Rates to 1% as Inflation Pressures Persist

BOJ Raises Interest Rates to 1% as Inflation Pressures Persist

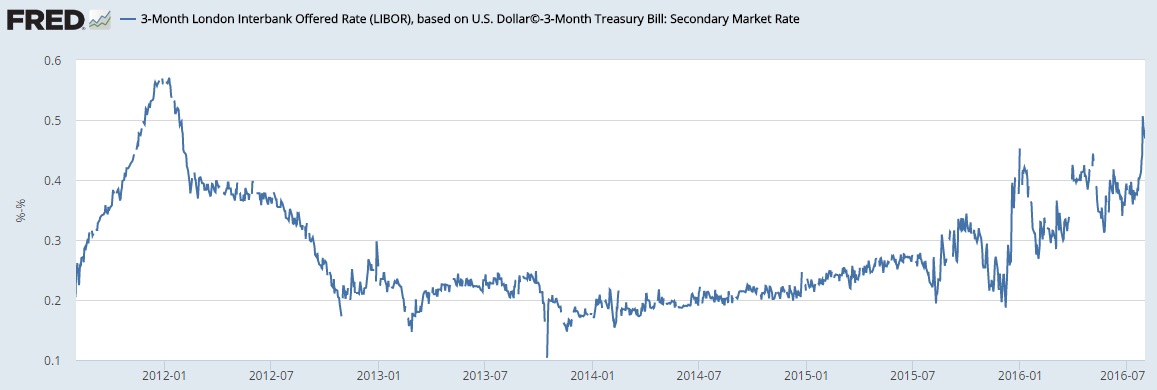

The cost of unsecured U.S. Dollar funding is creeping up and it has been creeping up since 2014, however, recent days have seen a relatively sharp jump in that cost not seen in years. The spread between the risk-free rates, which is treasury rate and the cost of unsecured funding (Libor) at which banks borrow from each other has moved to the highest level in more than four years. The spread is currently hovering around 50 basis points, which is highest since January 2012. If that spread past beyond 57 basis points, which we think it will, that would be the highest since the 2008/09 crisis.

This spread, which is popularly known as TED spread, was at 33 basis points in February 2007, from where it jumped above 2 percent by the end of the year and reached 3.16 percent at the peak of the crisis. This time, however, we feel that there could be chronic shortages of the dollar funding, which would lead to the rise in the spread but relatively slowly.

It is also important to note that, since the financial crisis, record easing from the U.S. Fed led to the formation of a close relation between the effective federal funds rate and Libor but if the new trend persists and the spread kept widening it would imply that despite all the easing Fed has lost its grip on the risk premia in the market. A large part of the blame could also be attributed to the new regulatory framework that has led to the shrinkage in dollar-based funding available via money market funds.