RBI Hits Pause as Geopolitical Storm Clouds Gather

RBI Hits Pause as Geopolitical Storm Clouds Gather  BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks  RBNZ Holds Interest Rates Steady but Signals More Hikes Ahead in 2026

RBNZ Holds Interest Rates Steady but Signals More Hikes Ahead in 2026  BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure

BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure  RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  South Korea Central Bank Holds Interest Rates Steady Amid Inflation Concerns

South Korea Central Bank Holds Interest Rates Steady Amid Inflation Concerns

As Russia was the earliest of a group of commodity-oriented emerging market economies to abandon the peg, the current turmoil has not surprised Russian markets, neither has the spike in the rouble's volatility, which has risen to the level seen in May 2015, although it is still far from the elevated level of January 2015.

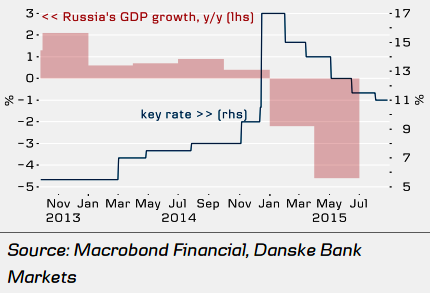

This time, the central bank of Russia (the CBR) is staying on the sidelines, resisting FX or even verbal intervention in order to avoid the risk of losing credibility.

"The renewed fall of the rouble will halt CPI growth deceleration and may push consumer prices further in the short run. Thus, the CBR is expected to halt its rate cuts on 11 September", says Danske Bank.

However, possible price increases will not be as dramatic as in early 2015, when the December 2014 devaluation was transferred into consumer prices. During 2015, the CBR has been consistent in its monetary policy, cutting its key rate by 600bp YTD as consumer price growth slowed and inflation expectations have eased on a stabilised rouble, after peaking at 16.9% y/y in March 2015.

"The CPI is expected to post 11% y/y in December 2015 on a high base effect and falling economic activity", added Danske Bank.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

CBR set to halt monetary easing

Thursday, August 27, 2015 4:19 AM UTC

Editor's Picks

- Market Data

Most Popular