Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

In March, we expect the German trade surplus to have amounted to €21.9bn, up from €19.5bn in February. Exports are expected to have increased by 0.2% MoM, following the rise of 1.4% MoM in February (-2.1%), while imports are expected to have decreased by 0.4% MoM, in line with signs of weak retail sales.

In Europe, Manufacturer's PMI for April that France and Greece produced readings of below 50.0 for the month, demonstrating an accelerated decline in factory production. Germany delivered a final reading of 52.1, Spain and Italy produced readings of 53.8 and 54.2 respectively. Currency traders await a general election on 7th May to elect the 56th Parliament of the United Kingdom.

While export data remain suppressed, temporary weakness in China linked to the New Year and in the US linked to weather and industrial action has probably distorted data temporarily in Q1. The weakening in Q1 exports looks particularly noteworthy in view of the significant weakening of the euro last year.

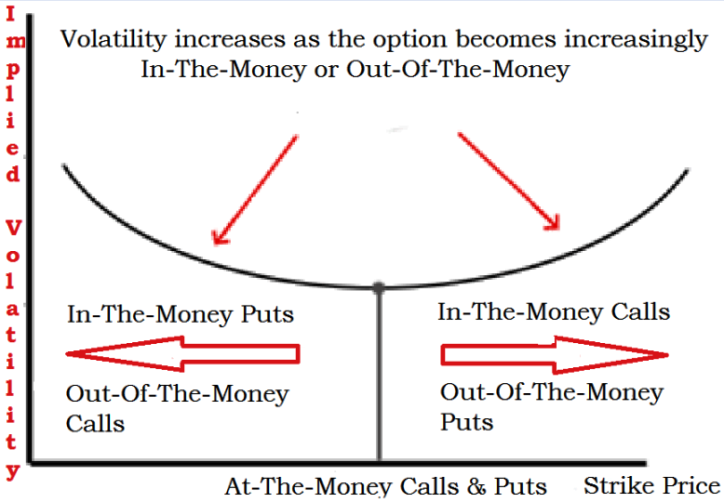

Increasing Implied volatility and Risk Management through currency derivatives:

Futures and Options contracts are highly useful in hedging purpose. But using the concept of Implied Volatility, one can determine whether a certain Call or Put is relatively expensive or cheaper.

Implied Volatility is the current Volatility of the underlying currency implied in its observed Option Price.

Using the Black Scholes formula one can find out the Volatility value that would result in the model producing the Option price which is equal to current market price.

As volatility affects the price of an option contract, an over estimation of volatility will result in overpriced option and an under estimation resulting in underpriced option.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

China distorting German exports adding weakness to Euro growth

Tuesday, May 5, 2015 6:47 AM UTC

Editor's Picks

- Market Data

Most Popular