Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX

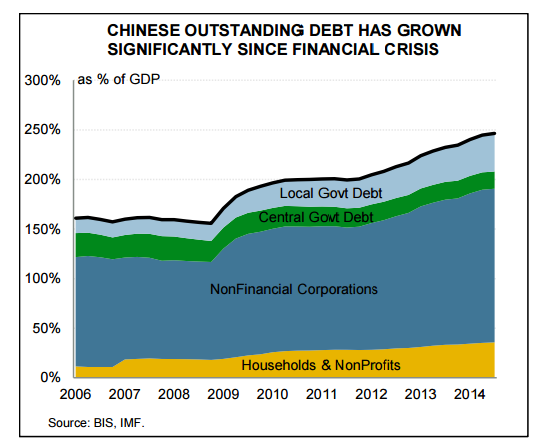

As swift as economic growth has been in China, credit growth over the last several years has been even more rapid. Following the financial crisis in 2008-09 and again as growth flagged in 2011 and 2012, China undertook large-scale credit-fuelled stimulus in order to boost its economy. This led to a surge in non-financial sector debt, which has grown from 156% of GDP in 2008 to roughly 250% of GDP at the end of 2014 - levels surpassing that in some advanced economies. On a sectoral basis, the biggest growth in debt has been within the non-financial corporate sector2 , where over-investment in many sectors has led to overcapacity.

This can only go on so long. The resulting debt overhang is already putting serious strains on the economy. Non-financial private sector debt was equal to 193% of GDP as of the fourth quarter of 2014. Simplistically assuming a seven-year rolling average of the weighted lending rate, the sector is currently spending roughly 12.1% of GDP on annual interest expenses alone. This is over 50% more than it was paying in early 2009. Lowering this debt burden would require deleveraging and/or lower interest rates. For this reason alone, further interest rate cuts from the People's Bank of China (PBoC) appear likely.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

China’s debt overhang is weighing on its economy

Thursday, July 23, 2015 10:17 PM UTC

Editor's Picks

- Market Data

Most Popular