SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns

Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

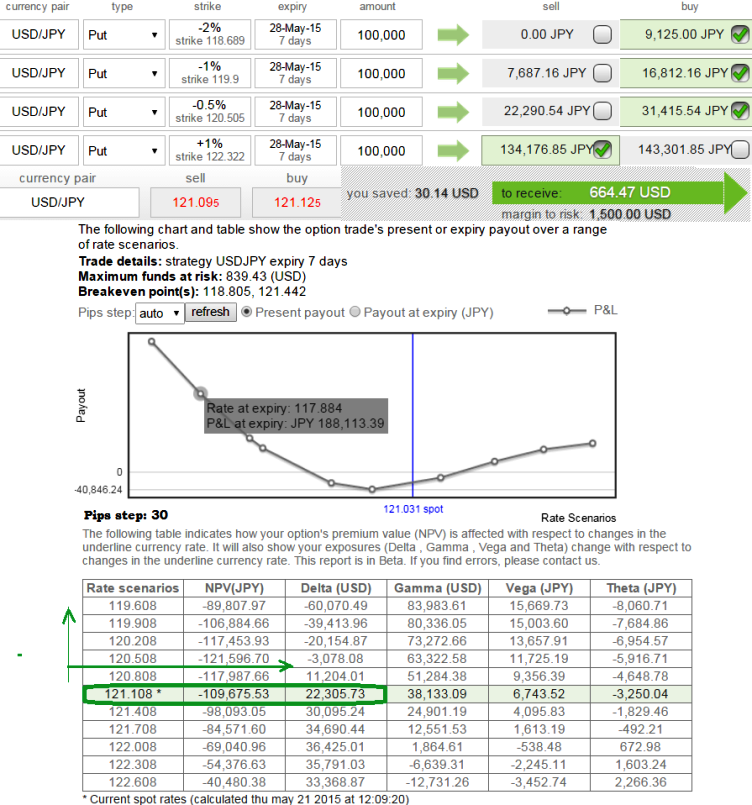

Arrest downside risks of USDJPY hedging through deploying option strategy: Put Ratio Back Spread

Expect the underlying currency cross (USDJPY in this case) to make a large move on the downside.

Purchase puts (OTM) and sell fewer puts of a higher strike (ATM or ITM) usually in a ratio of 2:1, 3:2 or 3:2.

This is more attractive and quite unusual strategy. Basically, you're selling an at-the-money short put spread in order to help pay for the extra out-of-the-money long put.

The higher strike short puts finances the purchase of the greater number of long puts and the position is entered for no cost or a net credit.

The underlying exchange rate has to make substantial move on the downside for the gains in long puts to overcome the losses in the short puts as the maximum loss is at the long strike.

Give it an adequate time to expiration so as to make a substantial move on the downside.

Delta advantage: As shown in the figure it is observed that the this strategy offers positive delta (22,305.73) at prevailing exchange rate which means we are long on USDJPY in underlying market. So, we are participating in dollar as long as it holds its strength but when JPY gains appreciation delta turns into negative (-3,078.08) which means we are also participating on downswings as well.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Delta advantage on Put Ratio Back Spread of USDJPY

Thursday, May 21, 2015 7:25 AM UTC

Editor's Picks

- Market Data

Most Popular