BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei

BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei  Indian Government Bonds Seen Opening Steady Ahead of RBI Policy Decision

Indian Government Bonds Seen Opening Steady Ahead of RBI Policy Decision  Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  RBNZ Holds Interest Rates Steady but Signals More Hikes Ahead in 2026

RBNZ Holds Interest Rates Steady but Signals More Hikes Ahead in 2026  ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks  Kevin Warsh Faces Early Fed Test as Inflation Risks Challenge Rate-Cut Expectations

Kevin Warsh Faces Early Fed Test as Inflation Risks Challenge Rate-Cut Expectations

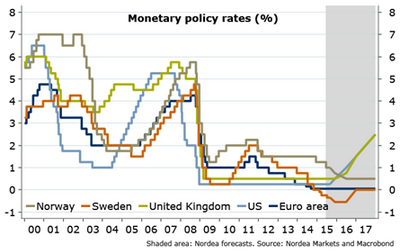

The ECB started to buy public sector bonds in March this year and intends to do so at least until September 2016. As it is seen, inflation by then will not be close enough to the 2% target and inflation expectations will not yet be "well anchored". Therefore, the ECB is expected to go on buying assets beyond September 2016.

"A half-year extension of the programme combined with an additional tapering period looks like a rather good first guess of how the purchase programme could evolve beyond September 2016. We expect the main refi rate to remain unchanged at 0.05% over the forecast horizon and the deposit rate to stay unchanged at -0.20%. For the next few months, the risk to our no-change baseline call is tilted towards more stimulus from the ECB", says Nordea Bank.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

ECB to support recovery for long time

Wednesday, September 9, 2015 5:49 AM UTC

Editor's Picks

- Market Data

Most Popular