Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war  Same sparkle, different story: how lab-grown diamonds are transforming the market

Same sparkle, different story: how lab-grown diamonds are transforming the market  Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring

Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring  Tech Stock Positioning Nears Neutral as Investor Rotation Enters Final Phase, Deutsche Bank Says

Tech Stock Positioning Nears Neutral as Investor Rotation Enters Final Phase, Deutsche Bank Says  ‘Vibe coding’ is fun and easy, but there’s a major catch

‘Vibe coding’ is fun and easy, but there’s a major catch  Gold Spikes to $4085 on Fed Pause as Traders Eye Sell-the-Rally Setup

Gold Spikes to $4085 on Fed Pause as Traders Eye Sell-the-Rally Setup

Since World War II, the average length of time between recessions is 5 to 6 years. With the current cycle clocking in at 81, it's natural to wonder if the next downturn is imminent.

Global inflation has begun to reflect recessionary levels (around 1% Y/Y change).

Global trade has collapsed as reflected by the 80% drop over the last 18 months.

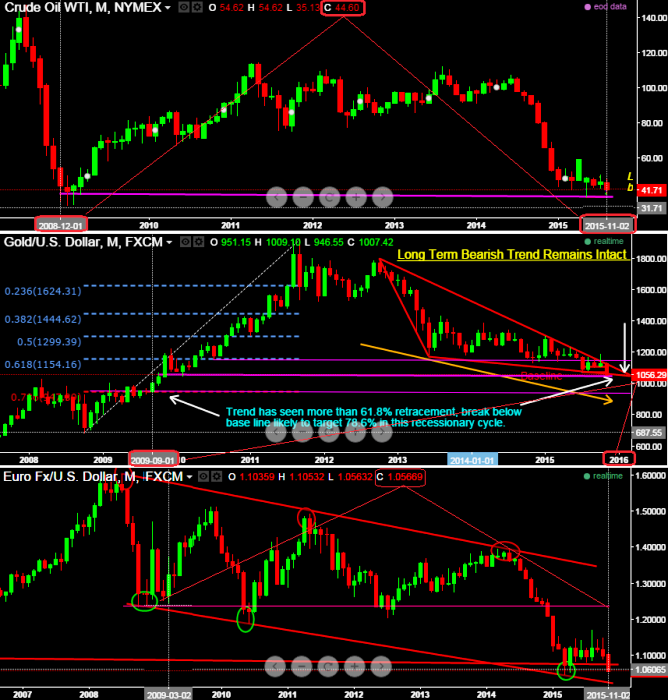

Declining trend over various asset classes (Bullion, crude and equity indices); compare the current levels with 2008 when last recession took place (see technical charts).

Recessionary trends are appearing in overall US imports/exports.

China's economy appears to be turning recessionary, recent currency devaluation has been the evidence so as to protect their economy.

In Germany, Europe's strongest economy, exports fell 5.2% in August from the previous month, growth momentum for been in the recessionary mode.

Japan already seems to have entered into the recessionary phase; industrial output disappoints projections (1.4% versus forecasts 1.9%).

It seems that the slow growth in snail's pace is only a momentary result of the 2008 financial crisis is absurd, this is no room for complacency.

The latest data suggest growth is slowing in the United States, and it is already slow in Europe and Japan. A global economy near stall speed is one where the primary danger is recession.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Flurry of reasons to ponder over global markets sensing recessionary phase

Monday, November 30, 2015 12:31 PM UTC

Editor's Picks

- Market Data

Most Popular

1