China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings

Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning

Japan Economy Minister Downplays Inflation Risks Despite BOJ Warning  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields

Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields  BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning

BOJ Seen Holding Rates at 1% While Keeping Inflation Risk Warning

The majority of the Aussie pairs are dragging price dips today on the back of the Chinese domestic demand saw a broad-based easing in April.

AUDUSD dipped -0.20%, EURAUD climbs +0.27%, while AUDJPY slipped about -0.37%, and so is AUDNZD (down by -0.11%).

Advances in retail sales decelerated from 8.7% YoY in Mar to 7.2%, the slowest growth since 2003.

Industrial production and investment fell to 5.4% and 6.1% (YoY YTD) from 8.5% and 6.3%.

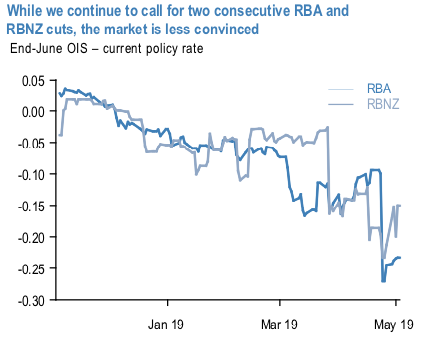

We now run you through the focus for antipodeans, of course, is on the central bank meetings that went on last week, in which we expected the first of two consecutive cuts for each central bank, out of which RBNZ has delivered. We still maintain that cutting expectations are justified by the RBA at this juncture, as a combination of household deleveraging, falling home prices and softening inflation is dragging on growth outcomes and raising real rates.

Market pricing suggests lesser conviction, however, as evidenced by some recent equivocation in short-dated OIS rates following the precipitous post-CPI drop from two weeks ago (refer above chart). Market odds of a cut are now just under 50% whereas we believe the proper odds are closer to 70%. This should open up yet further AUD downside if realised.

Benchmarking current expectations from the OIS market against our two-cut forecast by June indicates just how much potential downside there is in AUD rates which should lead to a sizable, one-sided widening in USD-AUD rate spreads given the Fed's dismissal of a near-term insurance cut.

Indeed, should the RBA cut next week, we would expect that to force the market to accept the likelihood of yet another cut and the prospect of a terminal policy rate that is below 1%.

We express this view both against the dollar in cash and against JPY in options encompassing the next two meeting dates – the latter funded by selling a USDJPY put which remains at historically low realized vol. Aside from the RBA deciding to play for time and not cutting next week, the main threat to bearish AUD positions would be from a resolution to the ongoing US-China trade talks.

Nevertheless, AUD is becoming less sensitive to Chinese developments and we would expect this to remain the case in the event of the RBA commencing an independent easing cycle.

Trade recommendations:

Long a 6w 76.75 AUDJPY put, short a 6w 110 USDJPY put. Paid net premium of 25bp at the end of April 25th. Marked at 26bp.

Stay short AUDUSD from 0.7090 March 4th. Marked at 1.28%. Courtesy: JPM

Currency Strength Index: FxWirePro's hourly AUD is flashing at -32 levels (bearish), while hourly JPY spot index is at 45 levels (which is bullish) while articulating at (07:38 GMT).

For more details on the index, please refer below weblink: http://www.fxwirepro.com/currencyindex