Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening

South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation

RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation  Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings

Eurozone Bond Yields Fall as Oil Slump Eases Inflation Fears Ahead of Central Bank Meetings  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

This week’s Australian CPI result was a significant surprise, with core inflation dropping to a 3 year low, alongside broad weakness in services pricing. We have been expecting the RBA to cut in July and August, motivated mostly by concerns about the activity data. But with inflation now drifting even further off track, we have brought this forward to cuts in May and June (25bp each), on the grounds that the Bank will be unable to defend a SoMP forecast set showing a return to the target without immediate policy action.

AUDUSD has been weakening since mid-month, and got a kick along from the CPI result, but has proven relatively sticky at the lower end of the six-month range, particularly in the context of fairly likely near-term easing (May OIS is currently priced at 50% for a cut). The market’s reluctance to embrace deeper downside in AUD partly reflects the background support from high commodity prices, and particularly, evidence of an upturn in China.

This was confirmed by the trimming of AUD shorts in last week’s IMM report, which coincided with stronger Chinese growth and IP data.

Still, in the absence of a broader Asia-wide recovery in the industry, further upside to Australia’s terms of trade is limited. And with rate differentials now finally starting to break the range (the move so far this year has only been a catch-up to the Fed), the beta to further incremental interest rate changes from the RBA is likely to be greater.

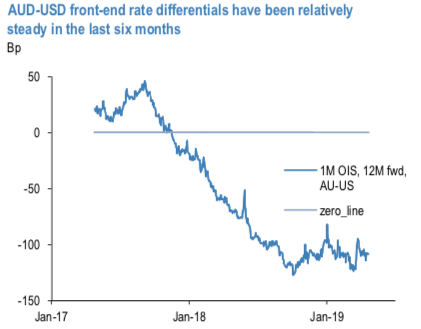

Relative AUD-USD policy expectations (12M fwd 1M OIS) have been range-bound at around -110bp over the last six months (refer above chart), having trended down by 170bp over the prior year. Alongside the resilience in iron ore prices, the recent sideways drift in rate spreads helps account for the stability of AUD since late 2018. Through the 2018 decline, AUDUSD had a beta of about 0.06 to AU-US rate differentials (% per bp).

Extension of this bout of RBA re-pricing is likely to take the form of a deeper market reassessment of the terminal rate, which has started pushing sub-1%. We are forecasting AUDUSD to 0.68 at mid-year. Given the partial beta mentioned above, and our Fed view, this AUD forecast would be consistent with an RBA terminal rate of 0.65%.

Trade tips:

Our largest exposures are short antipodes. We increase the beta ahead of potentially landmark policy decisions from the RBA and RBNZ in May, this time through an AUDJPY put part funded by selling a USDJPY put USDJPY implieds may be close to record lows but the risk premia are nevertheless high.

Buy a 6w 76.75 AUDJPY put, sell a 6w 1110 USDJPY put.

Buy USDINR 1Y ATM straddles vs sell AUDUSD 1Y straddles. Courtesy: JPM

Currency Strength Index: FxWirePro's hourly AUD spot index is inching towards -79 levels (which is bearish), while hourly USD spot index was at 50 (bullish), and JPY is at 67 (which is bullish) while articulating (at 09:02 GMT).

For more details on the index, please refer below weblink: http://www.fxwirepro.com/currencyindex