Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Morgan Stanley Says China’s Reusable Rocket Progress Poses Long-Term Challenge to SpaceX

Morgan Stanley Says China’s Reusable Rocket Progress Poses Long-Term Challenge to SpaceX  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Jamie Dimon Warns Anthropic's Mythos AI Poses National Security Risks

Jamie Dimon Warns Anthropic's Mythos AI Poses National Security Risks  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Morgan Stanley Downgrades Adobe, Workday as AI Transition Raises Growth Concerns

Morgan Stanley Downgrades Adobe, Workday as AI Transition Raises Growth Concerns  Morgan Stanley Names Marks & Spencer Top European Retail Pick, Sees Strong Upside

Morgan Stanley Names Marks & Spencer Top European Retail Pick, Sees Strong Upside  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Sterling was little changed yesterday despite lack of evidence on progress in Brexit negotiations. It has a very light data calendar for the day with nothing of note in the UK or the Eurozone. That is likely to result in UK politics and in particular Brexit negotiations remaining the key focus for markets. However, as yesterday’s meeting between Brexit Minister Raab and EU Chief Negotiator Barnier did not go ahead, it suggests they are still some way from a breakthrough.

Well, we reprise an investigation of sterling volatilities as carried out in an earlier piece. The value of owing optionality for hedging Brexit risk is confirmed.

We update an analysis on sterling volatility as carried out in an earlier piece, following weeks characterized by Labour/Conservative party conferences and UK/EU verbal tensions on the Brexit negotiations.

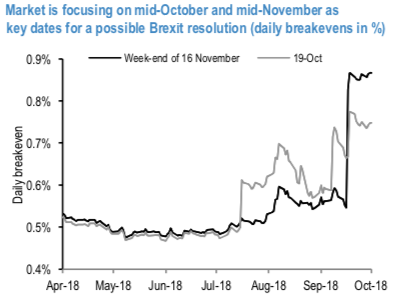

A smooth and upward sloping cable curve indicates the lack of specific risk-events especially in the 3M-1Y segment (where the curve is remarkably flat). If ever, over the past few weeks market attention has increased for the 19 October (EU summit) and mid-November (refer 1stchart), showing the daily breakevens); while an emergency November EU summit hasn’t been announced yet (that would be conditional on substantial progresses in the negotiations to occur in October), markets are closely watching the weekend of 16 November.

While vols have been on the rise since September, they remain very contained compared to the 2016 highs (refer 2ndchart for the 9M maturity): same conclusions are found for the so-called “vol of vol” parameter, which drives the convexity of the smile and the (implied) probability of fat-tail risk events to occur. The widening of risk-reversals in favour of GBP puts / USD calls (by around 1 vol) has been possibly more remarkable. Courtesy: JPM

Currency Strength Index: FxWirePro's hourly GBP spot index is inching towards 102 levels (which is bullish), hourly USD spot index was at 35 (bullish), while articulating (at 14:16 GMT). For more details on the index, please refer below weblink: