Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow

BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields

Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist

Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist  Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure

Australia Inflation Cools as Core CPI Misses Forecasts, Easing RBA Rate Hike Pressure  RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation

RBA Signals More Rate Hikes Possible as Australia Battles Stubborn Inflation  Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

Singapore Central Bank’s Exchange Rate Policy Explained: Why MAS Uses the S$NEER Instead of Interest Rates

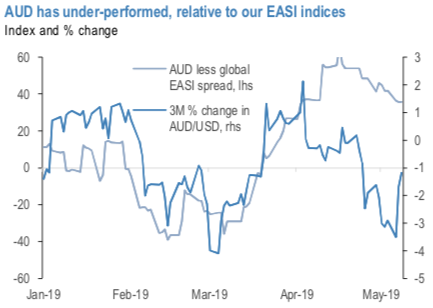

Despite local data continuing to out-perform relative to the global data flow (refer 1stchart), AUDUSD has under-performed of late, kept in check by a slow-burning negative domestic narrative, a re-escalation of trade war risks and the RBA’s gradual progression towards a more dovish policy stance.

Indeed, the RBA took another step towards a dovish policy bias this week, when it adjusted the last paragraph of its monthly Statement. We had expected the RBA to cut rates in May in light of the weak 1Q CPI data, but in the end this proved not to be a strong enough trigger.

Still, it can be argued that the RBA took a step towards rate cuts this month; previously, the Bank had indicated that a rising unemployment rate would be necessary to guarantee rate cuts. Now, improvement in the labour market appears to be a necessary condition for policy stability. This is clearly a weaker pre- condition for easing, and we now expect 25bp of easing in August, followed by another 25bp in November.

Consequently, the market is still priced for rate cuts (refer 2ndchart), which has kept pressure on front end rate differentials as the Fed has pushed back against the idea of an insurance cut.

The contrarian view on AUD of late has been that a combination of Chinese stimulus and good news on US-China trade relations will be supportive of the currency. Recent developments on this front have been mixed; generally China data has printed with a better tone, and last month our Chinese economists revised up their 2019 calendar year forecasts for Chinese growth to 6.4% (from 6.2%). But news on the US/China trade deal has soured this week, with heightened risk the US announces an increase in tariffs on $200bn of Chinese imports.

The majority of the Aussie pairs are dragging price dips today on the back of the Chinese domestic demand saw broad-based easing in April.

AUDUSDdipped -0.20%, EURAUDclimbs +0.27%, whileAUDJPYslipped about -0.37%, and so is AUDNZD(down by -0.11%).

Advances of retail sales decelerated from 8.7% YoY in Mar to 7.2%, the slowest growth since 2003.

Industrial production and investment fell to 5.4% and 6.1% (YoY YTD) from 8.5% and 6.3%.

We will now shed some light on the OTC outlook of AUD, before proceeding further into the options strategic framework.

Please be noted that the positively skewed IVs of 3m tenors signify the hedgers’ interests to bid OTM put strikes upto 0.67 levels which is in line with the above bearish scenarios (refer IV nutshell).

Please also be noted that mounting numbers of bearish risk reversals and bearish neutral RRs of the 3m tenors that are also in sync with the bearish scenarios refer (Refer risk reversal nutshell).

Overall, AUD OTC hedgers’ sentiments substantiate that their risk mitigating activities for the downside risks have been clear. Courtesy: Sentrix, JPM & Saxobank

Currency Strength Index: FxWirePro's hourly AUD is flashing at -20 levels (mildly bearish), while hourly USD spot index is at 2 levels (which is absolutely neutral) while articulating at (10:44 GMT).

For more details on the index, please refer below weblink:http://www.fxwirepro.com/currencyindex