US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate

Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation

SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be

Is Netanyahu’s star waning in Washington? His latest meeting with Trump suggests it may be  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

and EUR/RUB (options structures) - EconoTimes)

We choose RUB as the long leg of the trade to help offset the expensive carry costs of a short TRY position. RUB valuations are likely to be relatively steady over the coming months, on a mix of factors: (+) stronger current account surplus and likely further inflows into RUB denominated government bonds vs. (-) expected normalization of oil prices and higher external debt payments closer to year-end. Politics, as always, are a wild card.

JPM Commodities research has raised their oil forecasts for 2018 based on better-than-anticipated compliance to supply quotas, the likelihood of the OPEC/NOPEC production cut accord being extended through 2018, and a solid rise in global oil demand next year. As a positive current account oil exporter, RUB is the cleanest FX beneficiary of a bullish shift in oil prices and has added tailwinds of high rate carry and cleaner positions/cheaper valuations than earlier in the year that prompted our EMEA team to turn OW last month. We like expressing leveraged bullish RUB views via EURRUB instead of USDRUB for three reasons:

1) The better insulation to higher Treasury yields / stronger dollar;

2) The dovish tinge to the October ECB may have trimmed upside risks to the Euro, and Italian elections next year could potentially even generate some alpha on short EUR crosses in 1H’18 by refocusing investor attention on European sovereign risks; and

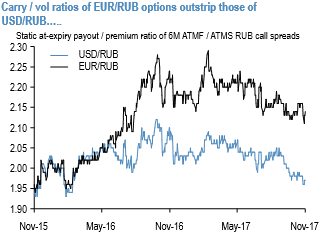

3) The carry/vol ratios of EURRUB options significantly outstrip those in USDRUB (refer above chart). RUB call spreads / at-expiry digitals are ideal formats to express leveraged views in given the weight of existing positions that are likely to sponsor a low volatility grind higher in the currency.

In addition, RUB risk reversals have been chronic underperformers this year, which is likely to continue in an environment of contained volatility and potentially stronger oil prices than we are budgeting for (hence outperformance of RUB calls on skews), so there is value in net earning premium by selling RUB puts for financing purposes even with highly asymmetric strike selections (refer above chart).

For instance, 6M 67 strike (1%OTMS) EUR put/RUB call at expiry digitals can be purchased vs. selling 6M 72 strike EUR call/RUB put at expiry digitals(6.4% OTMS, above 1-yr spot highs) @ 6.2% / -4.2% (i.e. net premium intake) of equal EUR notional/leg(forward ref. 70.49).

Short TRY-RUB spot exchange rate, we recommend a short TRY-RUB position, currently fixing rate trading at 15.3968. We target a 7.5% move lower to 14.5305 and place a stop loss at 16.1799. Our trade horizon is 6-9 months. The position costs about 37bp per month in carry.