S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

In Canada, November real GDP expected to rebound 0.4% MoM.

Q4’16 real GDP still tracking our 1.3% QoQ, forecast.

Wholesale sales softer than expected in November.

CMHC issues warning to homebuyers in overheated housing markets. The activity data in hand point to a solid rebound in November real monthly GDP growth. After a very weak start to the quarter with a 0.3% MoM decline, we expect it jumped 0.4% MoM in November.

However, preliminary estimates of December exports point to softer real GDP growth in the month. All in, we maintain our Q4’16 real GDP forecast of 1.3% QoQ.

In the current quarter, the recent surge in the PMI orders and export orders indexes supports our call for growth to accelerate to 2.3% QoQ.

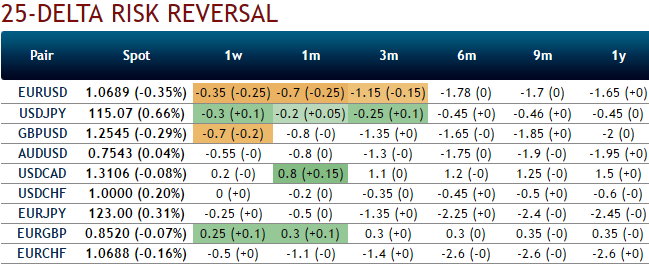

OTC outlook:

As you could observe the risk reversal flashes across all tenors, although we see neutral changes to the bullish risk sentiments, as a result, CAD seems to be gaining in next 2 months tenor on recent OPEC’s announcements, but on the contrary, USD’s robustness seems more attractive than CAD on account of series of significant events such as the Trump’s oath taking ceremony is nearing and on the Fed’s chances of hiking in 2017 can certainly not be disregarded.

Moreover, all these factors are discounted in FX option market. You could make out this in mounting risk sentiments as you could see the positively skewed IVs in OTM call strikes.

Well, these positive skews in 2m implied volatilities suggest RKO calls on both hedging as well as speculative grounds, the USDCAD 2-3m skew has been well bid with Trump progresses in the beginning months to come, lifting it to its highest level since June 2015.

We reckon the above fundamentals seem to be reasonably addressed by hedging participants, hence, we advocate below option strategy to mitigate risks on either way with cost effectiveness.

Hedging Framework:

Strategy: 2m 3-Way Diagonal Straddle versus OTM Put

Spread ratio: (Long 1: Long 1: Short 1)

Rationale: Let’s glance on sensitivity tool for 2m IV skews would signify the interests of OTM call strikes that means the ATM calls higher likelihood of expiring in-the-money, so writing overpriced OTM puts would be a smart move to reduce hedging cost.

The execution:

Go long in USDCAD 1M at the money -0.49 delta put, and go long 2M at the money +0.51 delta call and simultaneously, Short 2W (1%) out of the money put.