Major Pair Currency Score: NZD/USD and AUD/USD Lead Forex Rally with Perfect 100 Scores

Major Pair Currency Score: NZD/USD and AUD/USD Lead Forex Rally with Perfect 100 Scores  EUR/USD Rockets Past 1.1560 as Soft U.S. Jobs Data Fuel Fed Rate-Cut Surge

EUR/USD Rockets Past 1.1560 as Soft U.S. Jobs Data Fuel Fed Rate-Cut Surge  DAX & CAC40 Score Perfect 100: Extremely Bullish With Major Levels to Watch as FTSE100 Hits 80

DAX & CAC40 Score Perfect 100: Extremely Bullish With Major Levels to Watch as FTSE100 Hits 80  Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring

Meta-backed research finds exposure to ‘untrustworthy’ social media is rare. The fine print is less reassuring  FxWirePro: EUR/AUD slips after surprise U.S. employment data

FxWirePro: EUR/AUD slips after surprise U.S. employment data  FxWirePro: NZD/USD retreats as Middle East instability weighs

FxWirePro: NZD/USD retreats as Middle East instability weighs  FxWirePro: GBP/USD rises as weak U.S. jobs data pressures dollar

FxWirePro: GBP/USD rises as weak U.S. jobs data pressures dollar  FxWirePro : EUR/NZD slips lower after soft US jobs report

FxWirePro : EUR/NZD slips lower after soft US jobs report  FxWirePro: USD/ZAR gains some ground, but downtrend remains

FxWirePro: USD/ZAR gains some ground, but downtrend remains  FxWirePro: USD/CNY slips as strong China exports data Lift yuan

FxWirePro: USD/CNY slips as strong China exports data Lift yuan  Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate

Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate  Bitcoin Reclaims $65,000 as Easing Geopolitical Tensions Fuel Risk-On Rally

Bitcoin Reclaims $65,000 as Easing Geopolitical Tensions Fuel Risk-On Rally

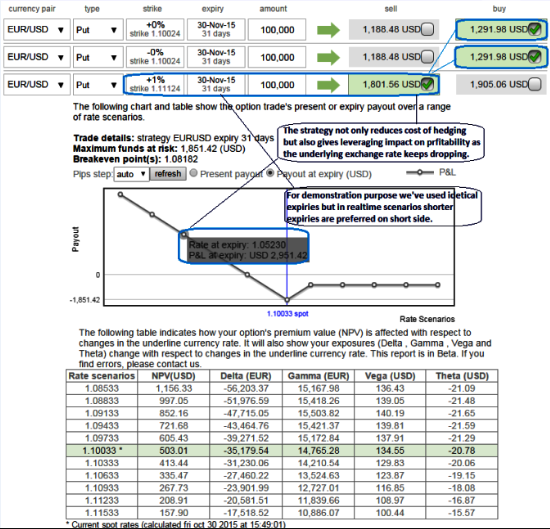

The delta risk reversal for 1m contracts have shown bearish signals back again and long term (1M-1Y) put contracts are also on higher demand.

While the pair is still to percieve the highest implied volatility for 1W at the money contracts among G7 currency space, almost nearing 12%, certainly rising higher which is favorable for those look for option writings.

With this qualitative reasoning, we recommend arresting further downside risks of this pair by hedging through Put Ratio back Spread.

Expect the underlying currencies EURUSD in this case to make a large move on the downside.

As shown in the figure purchase 1m 2 lots of At-The-Money -0.48 delta puts and sell 1w one lot of (1%) In-The-Money put option usually in the ratio of 2:1.

The short ITM puts funds to the purchase of the greater number of long puts and the position is entered for no cost or a net credit. The delta of combined positions should be around -0.34 with slightly negative theta value.

The underlying exchange rate has to make substantial move on the downside for the gains in long puts to overcome the losses in the short puts as the maximum loss is at the long strike. Give it a longer time to expiration so as to make a substantial move on the downside.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: Deploy EUR/USD PRBS to hedge spot FX downside risks

Friday, October 30, 2015 11:39 AM UTC

Editor's Picks

- Market Data

Most Popular