Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate

Gold Shines on Oil Relief: Buy Dips at $4160, Targeting $4305 as Bullish EMAs Dominate  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war

Ukraine’s drone strikes are having an impact on Russia — but Russian leaders remain committed to war  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation

SpaceX Earnings Preview: Bernstein Says 4 Key Factors Will Drive Long-Term Valuation  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  ‘Vibe coding’ is fun and easy, but there’s a major catch

‘Vibe coding’ is fun and easy, but there’s a major catch  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

- EconoTimes)

We do not chase the strong price action in higher yielding currencies and stay neutral on ZAR, TRY and RUB. EM local markets have staged an impressive rally in the past three months. The question for investors is whether or not to chase the strong price action in higher yielding currencies.

In EMEA EM local markets, we think the answer is ‘no’. Stretched risk premia, unattractive valuations and upcoming event risks (Fed, European politics) suggest the momentum of the rally has peaked for now. We, therefore, stay neutral in high yielding currencies. The conviction in bearish CEE FX positions is reinforced on underpriced European political risks in EM. A number of indicators suggest the EM FX rally is running out of steam, in our view:

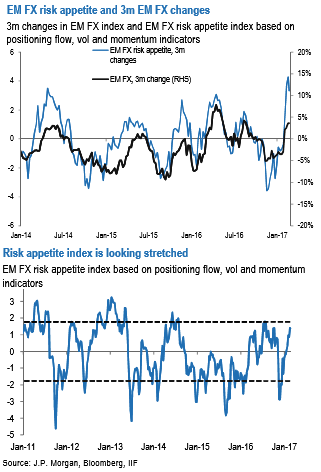

First, our EM FX risk appetite index looks increasingly stretched. The above charts show that the EM FX risk appetite index, based on a number of risk, flow and positioning metrics, is heading towards stretched levels. Historically, changes in this index have co-moved closely with EM FX. Admittedly, we have underestimated the extent to which risk appetite would recover from the lows in December, and have successively closed bearish EM FX positions (taking profits on TRY, and being stopped out of long USDRUB) in response.

Second, the performance of EM currencies has significantly diverged from the Dollar Index.

We believe that political risk into the French elections is priced more appropriately in bonds (but not in currencies) than going into the Brexit and US vote.

Higher yielding currencies are fair-value to expensive at current levels.

The histogram chart shows that EMEA EM currencies are currently either around the fair value (TRY and ZAR) or expensive (RUB) on the high-frequency models.

A positive % deviation indicates the USD/EM (EUR/EM) cross is trading too high; a negative % deviation indicates the USD/EM (EUR/EM) cross is trading too low. Deviations are from “intuitive” short-term models.

As such, both top down and bottom up indicators point to there being little value in chasing the momentum in higher yielding currencies in EMEA EM.

Second, we also note that ILS, the only currency in EMEA EM on which we were bullish, is also looking expensive at current levels, which leads us to close out our EURILS put spread in profit upon expiry.